Cold calling distressed homeowners is one of the highest-leverage skills a real estate investor can develop. When someone faces foreclosure, probate, or divorce, they need options fast. But reaching them effectively takes more than a phone and a script. You need preparation, empathy, legal awareness, and the ability to have a real conversation under pressure. Cold calling response rates sit between 5 and 10%, already outperforming direct mail. With the right approach, those numbers get even better. This guide gives you everything you need to make calls that actually convert.

Table of Contents

- Key Takeaways

- Preparation before cold calling distressed homeowners

- Crafting scripts that actually connect

- Executing calls with timing, follow-up, and multi-channel support

- Troubleshooting common pitfalls

- Expected outcomes and how to measure results

- My honest take on cold calling distressed homeowners

- Practice smarter with Closersleague

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Preparation drives results | Know the distress type, verify contact data, and scrub your list before dialing a single number. |

| Empathy is your best opener | Consultative, education-first calls outperform pushy pitches with distressed sellers every time. |

| Compliance is non-negotiable | Scrub your list against the DNC Registry every 31 days or risk fines up to $51,744 per call. |

| Multi-channel follow-up wins | Cold calls work best inside a system that includes mail, SMS, and in-person follow-up. |

| Practice separates closers | Drilling scripts and objection handling in a safe environment builds the confidence that converts leads. |

Preparation before cold calling distressed homeowners

Most investors pick up the phone before they are actually ready. That mistake costs you deals. Solid preparation means you know who you are calling, why they may want to sell, and whether you are legally allowed to call them at all.

Know the distress type first

Foreclosure, probate, and divorce each create different emotional states and different timelines. A homeowner who just received a Notice of Default has more urgency than someone in a probate situation that could stretch 12 months. Federal law prohibits foreclosure until a borrower is 120 days delinquent, which means there is often a meaningful window to reach someone before they run out of options. With foreclosure filings rising 12% year-over-year in April 2026, the pool of distressed leads is growing. Understanding the timeline for each distress type shapes everything about how you open that conversation.

Build and verify your lead list

Accurate data is the foundation of productive outreach. Here is what your pre-call checklist should cover:

- Property ownership records pulled from county assessor or recorder databases

- Skip tracing to find current phone numbers (free directories go stale fast)

- Distress indicators such as Notice of Default filings, tax delinquency, or probate court records

- DNC Registry scrub completed within the last 31 days

- Verified property details including address, estimated equity, and time since distress event

Knowing property details before dialing is directly tied to better conversations. When you can reference specific facts, you stop sounding like a random robocall and start sounding like someone who actually knows their situation.

Stay legally compliant from day one

The FTC Telemarketing Sales Rule carries serious teeth. Scrubbing against the National DNC Registry must happen at least every 31 days, with fines reaching $51,744 per call for violations. One common mistake is treating compliance as a one-time setup. It is not. DNC compliance requires ongoing scrubbing because phone numbers get reassigned and consumers join the registry at any time. Run your own scrubs. Do not rely solely on your data vendor to handle this.

Pro Tip: Keep a compliance log showing the date of each DNC scrub, which list was used, and who performed it. This documentation is your Safe Harbor protection if a complaint is ever filed.

Crafting scripts that actually connect

The single biggest script mistake investors make is writing something that sounds like a sales pitch. Distressed homeowners suffer decision fatigue from robocalls and mailers. If you sound like everyone else, they hang up before you finish your second sentence.

The four phases of an effective call

Think of every call as moving through four stages, not just opening and closing.

- Introduction. State your name, why you are calling, and that you work in the area. Keep it to two sentences. Do not mention buying yet.

- Discovery. Ask open questions to understand their situation. “Have you had a chance to speak with anyone else about your options?” and “How long have you owned the property?” open people up fast.

- Tailored solution. Only after listening do you introduce what you offer. Frame it around protecting their credit, avoiding a public auction, and getting some control over their timeline.

- Next steps. End with a clear, low-pressure ask. A 15-minute follow-up call or a quick walkthrough of the property keeps momentum without feeling pushy.

Referencing public records builds instant credibility

Mentioning specific public record details like the Notice of Default date or the name of the lender signals that you are not reading from a generic list. It signals local expertise. A line like “I saw that a Notice of Default was filed on your property about 60 days ago” is far more powerful than “I understand you might be behind on payments.” One sounds researched. The other sounds scripted.

Handling objections with respect

You will hear “not interested,” “I already have an agent,” and “how did you get my number” on almost every session of calls. Here are the three principles that work:

- Validate first. “That makes complete sense” or “I totally understand” before any rebuttal keeps defensiveness low.

- Ask one more question. Instead of launching into a counter-argument, try “Can I ask what your main concern is right now?” This often reveals the real objection.

- Respect hard stops. If someone says they are not interested twice, thank them and move on. Persistence has limits. Respect builds your reputation.

Pro Tip: The discovery phase of a cold call is where most deals are won or lost. Spend more time asking and less time talking. A 70/30 listen-to-speak ratio during discovery dramatically improves rapport.

Executing calls with timing, follow-up, and multi-channel support

Good preparation and a solid script still need proper execution. When you call, how often you follow up, and what you do between calls all affect your conversion rate.

Best times to call and how many attempts to make

Research across sales industries consistently shows that mid-morning (between 9 and 11 a.m.) and late afternoon (between 4 and 6 p.m.) produce the highest answer rates. For distressed homeowners specifically, avoid Monday mornings and Friday afternoons. Most are dealing with week-start stress or checked out by Friday. Plan to make six to eight contact attempts per lead before retiring it. Many responses come on the fourth or fifth try.

Here is a practical call cadence to follow:

- First call on day one, morning.

- Second call on day three, late afternoon.

- Send a direct mail piece between days four and six.

- Third call on day eight.

- Send an SMS on day ten with a brief value message and your name.

- Fourth call on day fourteen, try a different time of day.

- Send an email with a foreclosure resource guide or helpful PDF.

- Final call attempt on day twenty-one before moving lead to long-term nurture.

Integrating calls into a multi-channel system

Systematic outreach beats one-off calls every time. When someone sees your letter in the mail, then gets a call from the same name, then receives a helpful text, you stop being a cold caller and start being a familiar presence. That recognition shift is what opens doors.

Contacting distressed sellers across multiple channels also lets each touchpoint reinforce the others. Your direct mail piece can reference that you will be calling. Your call can reference the letter. Your SMS can offer the PDF you mentioned on the call. Offering resources like foreclosure guides increases trust and keeps communication lines open between touches.

- Keep all outreach logged in a CRM, even simple notes on what was said and the homeowner’s tone

- Tag leads by distress type so you can customize follow-up messaging

- Never let a “not now” lead go cold without at least one re-contact at the 30-day mark

Troubleshooting common pitfalls

Even experienced investors hit walls. Usually, the problem is one of three things: too much hesitation before dialing, sounding robotic on the call, or ignoring compliance until it becomes a crisis.

Most investor failures come from over-analyzing leads before picking up the phone. You do not need perfect data to make a first call. You need enough. Do your research in layers: basic verification before the call, deeper research after you get a live conversation. This keeps your daily call volume up and your pipeline full.

Common mistakes that kill deals mid-call:

- Sounding scripted. If you are reading word-for-word, the homeowner hears it. Practice until the script becomes natural conversation.

- Using industry jargon. Terms like “as-is cash offer,” “ARV,” and “wholesale” mean nothing to most distressed homeowners. Speak plainly.

- Skipping empathy. Opening with your offer before understanding their situation signals that you only care about the deal.

- Ignoring compliance gaps. Relying entirely on your data vendor to handle DNC scrubbing is a compliance risk. Own the process yourself.

Pro Tip: Record your calls (with proper disclosure where required by state law) and review them weekly. Most investors are surprised by how often they interrupt, rush past objections, or miss cues that a homeowner was actually open to talking.

Expected outcomes and how to measure results

Understanding what good results look like helps you stay consistent instead of quitting too early.

| Metric | Benchmark | Notes |

|---|---|---|

| Answer rate | 10 to 20% of dials | Varies by list quality and time of day |

| Conversation rate | 40 to 60% of answered calls | Improves significantly with scripting practice |

| Lead to appointment | 5 to 10% of conversations | Consultative approach drives this higher |

| Appointment to contract | 20 to 30% | Depends on motivation level and your offer |

| DNC re-scrub interval | Every 31 days | Required for legal compliance |

Conversion from first contact to a signed contract with distressed sellers typically takes 30 to 90 days. Probate leads often take longer because legal processes do not move on your schedule. Set realistic follow-up cycles and use your CRM to automate reminder tasks so no lead ages out without a touchpoint.

Signs that a lead list has gone stale: high wrong-number rates, disconnected calls, and angry responses from people who sold the property months ago. When those signals appear, re-scrub, re-verify, and refresh with newer data before burning through more call time.

For pre-foreclosure and short sale situations, understanding the property’s current market value helps you have a more credible conversation with the homeowner about realistic proceeds and timelines.

My honest take on cold calling distressed homeowners

I have watched investors with pristine spreadsheets and zero closed deals. And I have watched others with messy notes and full pipelines. The difference is almost never data quality. It is willingness to have real, uncomfortable conversations with people who are scared.

In my experience, the investors who last in this business treat every call as a conversation, not a transaction. They genuinely want to help. That is not a soft skill. That is a competitive advantage. Homeowners in distress have talked to plenty of people who only care about the deal. When you show up differently, they notice.

What I have also learned is that compliance is not just legal housekeeping. I have seen investors who built solid pipelines lose everything because they ignored DNC rules for months. One complaint can trigger an investigation. The fines are not hypothetical.

My most practical advice: practice your calls before you make them. Not in your head. Out loud. With someone pushing back on you. The investors who roleplay their calls before dialing handle objections with confidence because they have already heard them twenty times. Stop winging it. Start drilling.

— Dave

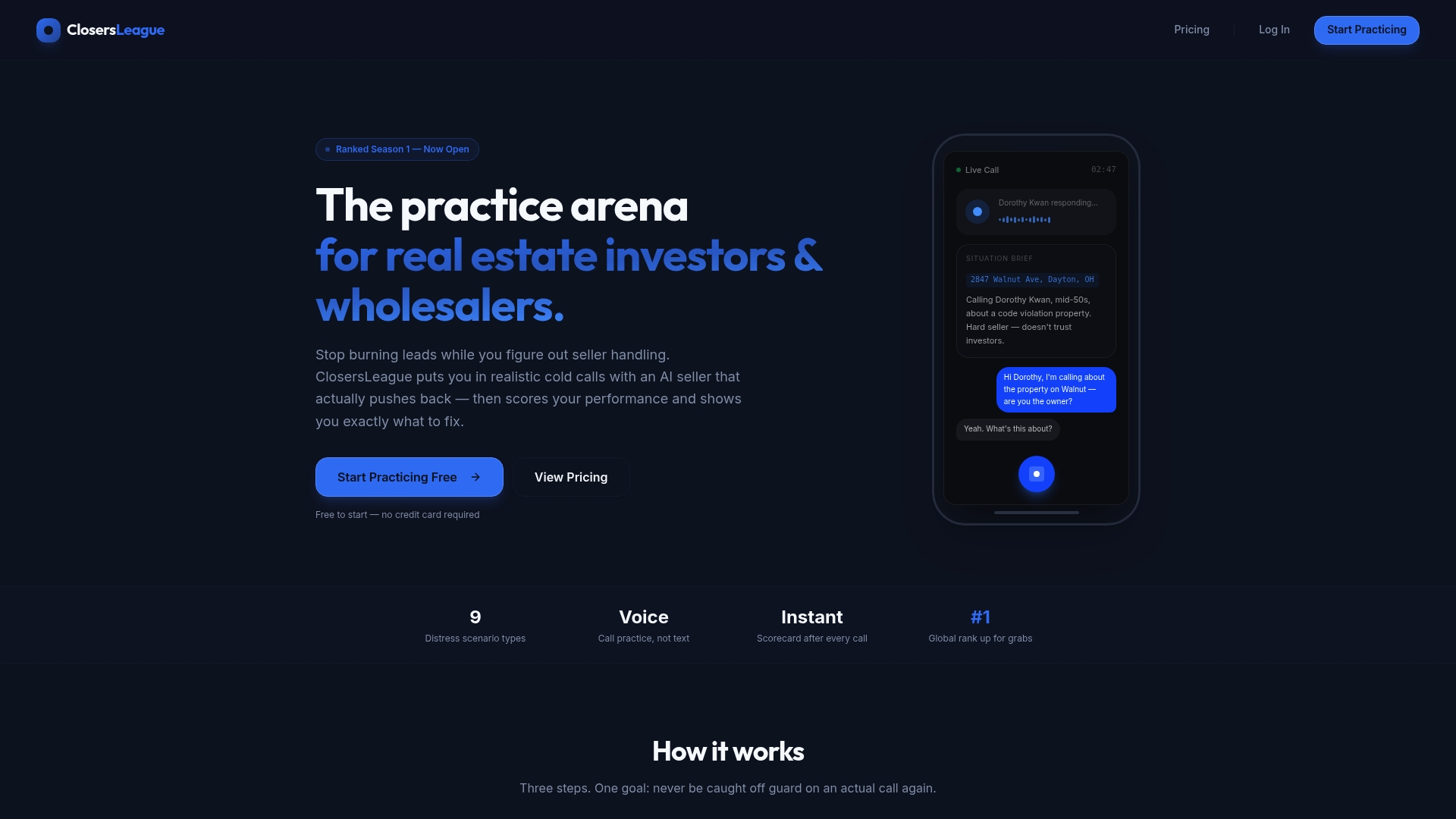

Practice smarter with Closersleague

Knowing the right approach is step one. Building the muscle memory to execute it under pressure is another challenge entirely. That is exactly what Closersleague is built for.

Closersleague is an AI powered cold calling training platform for real estate investors and wholesalers. You can practice foreclosure cold calling scenarios with an AI that pushes back like a real homeowner, score your performance, and build the consistency that converts leads. Whether you are working foreclosure, probate, divorce, or vacant property leads, Closersleague has roleplay scenarios designed for each distress type. If you are ready to stop losing deals on the phone and start closing them, explore all cold calling practice tools and put your skills to the test today.

FAQ

What is the best opening line for a distressed homeowner cold call?

Keep it brief and reference a specific detail from public records, like the Notice of Default date. Homeowners respond better when callers demonstrate local knowledge rather than using a generic pitch.

How often should I scrub my list against the DNC Registry?

You must scrub your lead list at least every 31 days. DNC violations carry fines of up to $51,744 per call, so ongoing compliance is a business-critical habit, not a one-time task.

How many times should I attempt to contact a distressed seller?

Plan for six to eight contact attempts before retiring a lead. Many responses come on the fourth or fifth try, especially when you combine calls with direct mail and SMS in a structured outreach sequence.

What is the average response rate for cold calling distressed sellers?

Cold calling distressed property leads generates response rates between 5 and 10%, which is significantly higher than direct mail at 1 to 3%. That gap grows when you lead with empathy and specific property knowledge.

How do I handle a distressed homeowner who says they are not interested?

Validate their response, then ask one open-ended question about their main concern. If they decline twice, thank them and move on. Respecting boundaries protects your reputation and often keeps the door open for a future call.