Choosing the right property acquisition strategies separates investors who build real portfolios from those who chase deals and wonder why the numbers never work out. In real estate, the formal umbrella term is “acquisition strategy,” and it covers everything from distressed asset purchases and wholesaling to long-term buy-and-hold approaches and complex tax-deferred exchanges. This guide breaks down the full spectrum of real estate investment methods, giving you the evaluation criteria, execution details, and comparison frameworks you need to match the right approach to your market, your capital, and your goals.

Table of Contents

- Key Takeaways

- 1. Understanding your criteria for property acquisition strategies

- 2. Fix and flip

- 3. BRRRR strategy

- 4. Buy and hold

- 5. Wholesaling

- 6. Tax deed and auction acquisitions

- 7. 1031 exchanges

- 8. Off-market sourcing with market data and cold outreach

- 9. Comparing acquisition approaches by investor profile

- My honest take on picking the right approach in 2026

- How Closersleague helps you source more deals

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Match strategy to conditions | Align your acquisition approach to current market inventory, absorption rate, and your own risk tolerance before committing capital. |

| Due diligence is non-negotiable | Title checks, environmental reviews, and unpaid tax searches determine whether a deal holds up after the offer. |

| BRRRR demands precise underwriting | Buying at 65–70% of ARV minus rehab costs is the minimum threshold to make the refinance exit work. |

| Data beats sentiment | Transaction velocity, days on market, and absorption metrics give you real negotiation leverage where social media buzz gives you nothing. |

| Cold outreach is a skill, not a numbers game | Consistent, coached cold calling to distressed sellers is one of the highest-ROI sourcing methods available to investors and wholesalers. |

1. Understanding your criteria for property acquisition strategies

Before you pick a method, you need a scoring framework. The four classic risk buckets that institutional investors use also apply to smaller operators: Core (low risk, stabilized assets, modest returns), Core-Plus (slightly more active management, modest upside), Value-Add (repositioning required, higher returns), and Opportunistic deals are the riskiest category and can take three or more years to generate returns.

Your risk profile should dictate which bucket you operate in. A first-year wholesaler and a seasoned fix-and-flip operator are not competing for the same deals, and they should not be using the same evaluation framework.

Key criteria to run through before any offer:

- Market conditions: Quantify transaction velocity and inventory using days on market, absorption rates, and vacancy timelines. These numbers tell you your negotiation leverage. Social media sentiment tells you nothing useful.

- Due diligence checklist: Environmental assessments, title checks, unpaid tax reviews, and physical inspections belong on every deal. Skipping any one of them is where most acquisitions go wrong.

- Valuation framework: Use fair-value triangulation combining comparable sales, yield models, and replacement cost. If the three inputs converge within 5%, you have high confidence. Divergence over 8 to 10% means you slow down and ask harder questions.

- Financial floor: Build your offer floor by subtracting defect costs explicitly. Your ceiling is the maximum allowable offer given your target return. Both numbers protect you from anchoring on the asking price.

- Operational fit: Can you manage a rehab, handle a 1031 timeline, or run a rental? Honest answers here prevent expensive mismatches between strategy and execution.

Pro Tip: Never rely on a single valuation method. Comps alone can mislead in thin markets. Adding a yield model and a replacement cost estimate takes 20 extra minutes and can save you from a six-figure mistake.

2. Fix and flip

Fix and flip is the most well-known of all property purchase techniques and the one most investors attempt first. You buy a distressed property at a discount, renovate it, and sell at market value within a short window, typically six to twelve months.

The math is straightforward: your profit equals sale price minus purchase price, rehab costs, carrying costs, and transaction fees. The execution is where most investors struggle. Rehab timelines slip. Contractor costs overrun. Markets shift between the day you buy and the day you list.

Target ROI for a well-executed flip is typically 15 to 20% of the after-repair value (ARV). To protect that margin, experienced flippers build in a contingency of 10 to 15% of their rehab budget before they submit an offer. They also pre-qualify buyers or line up agent relationships before closing on the purchase side.

Distressed properties are the primary sourcing pool here: foreclosures, probate sales, divorce-driven sales, and tax-delinquent properties. That is why cold calling motivated sellers is one of the most direct sourcing tools available. You reach people before the property hits any public list.

3. BRRRR strategy

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It is one of the most capital-efficient real estate investment methods when executed correctly, because the refinance step recycles your initial capital into the next deal.

The entry math is tighter than a flip. You need to buy at approximately 65 to 70% of ARV minus your full rehab cost to make the refinance appraisal work. Miss that threshold and you leave capital trapped in the deal. For a complete breakdown of each phase, the BRRRR acquisition process covers rental seasoning requirements and appraisal preparation in detail.

Three things most guides underemphasize about BRRRR:

- Refinance underwriting is the bottleneck. The rehab gets all the attention, but the lender’s appraiser determines whether your capital comes back. Understand their methodology before you start construction.

- Seasoning requirements vary by lender. Many lenders require six to twelve months of rental history before a cash-out refinance. Factor that timeline into your capital needs.

- Tenant quality affects your appraised value in some markets. Placing a reliable, market-rate tenant before the appraisal can support a higher income-based valuation.

4. Buy and hold

Buy-and-hold is the closest residential equivalent to Core investing. You acquire a property, stabilize it with a long-term tenant, and hold for cash flow and appreciation. The strategy rewards patience and penalizes short-term thinking.

The sourcing criteria differ from flips and BRRRR deals. You are less focused on deep discounts and more focused on rent coverage ratios, neighborhood trajectory, and long-term demand drivers like employment and population trends.

Distressed properties still fit here if the discount is sufficient to support a positive cash-on-cash return from day one. The management overhead, however, is real. Factor in property management fees (typically 8 to 12% of gross rents), vacancy allowances, and capital reserves for maintenance before you calculate returns.

5. Wholesaling

Wholesaling is a property purchase technique where you contract a distressed property at a discount and assign that contract to an end buyer, typically a rehabber or landlord, for an assignment fee. You never take title. Your profit is the spread between your contracted price and what your buyer will pay.

This makes wholesaling the lowest-capital entry point in real estate, but not the lowest-skill one. Your entire business runs on deal sourcing and seller conversations. You need a consistent pipeline of motivated sellers, and you need to convert those conversations into signed contracts at the right price.

The sellers you call are typically facing foreclosure, probate, divorce, inherited properties, or tax delinquency. Those conversations require real skill. A homeowner in financial distress does not respond well to a pitch. They respond to someone who understands their situation and offers a clear path forward. That is a trained skill, not a script.

6. Tax deed and auction acquisitions

Buying at tax deed auctions is one of the more aggressive land acquisition strategies and commercial property tactics available to experienced investors. When a property owner fails to pay property taxes, the county can eventually auction the property to satisfy the debt.

The opportunity is real. So is the risk. Tax deed acquisitions can carry title risk and surviving liens that require legal action to clear after the auction closes. Auction mechanics also move fast. Deposits are required, and payment schedules are short.

Two rules for auction buying: First, pull a title search before you bid, not after. Second, budget for a quiet title action in your holding costs. In some states, those legal proceedings take six to twelve months. In New Jersey, the Abandoned Property Rehabilitation Act removes the standard two-year wait for tax foreclosure on abandoned properties, which can accelerate your acquisition timeline if the property meets abandonment standards.

7. 1031 exchanges

A 1031 exchange lets you defer capital gains taxes by rolling proceeds from a sold property into a new acquisition. For investors scaling a portfolio, it is one of the most powerful tools in strategic real estate buying.

The mechanics are straightforward. The execution is unforgiving. You have 45 days to identify replacement properties and 180 days to close. Both are calendar days, not business days. Miss either deadline by a single day and you lose the tax deferral entirely.

Work with a qualified intermediary from the moment you go under contract on the sale side. Your exchange starts the moment the relinquished property closes, so there is no margin for slow coordination. Pre-identify two or three replacement properties before your sale closes so you are not scrambling under a 45-day clock.

8. Off-market sourcing with market data and cold outreach

Most profitable acquisitions never touch the MLS. The best ways to acquire property at a real discount involve finding motivated sellers before they list publicly. That means combining market data analysis with direct outreach.

On the data side, use price bands, days on market, and absorption rates to identify neighborhoods where sellers have the most pressure and the least leverage. These metrics tell you where to focus your outreach energy, not just where prices are falling. You can read more about using transaction velocity for sourcing in competitive markets.

On the outreach side, cold calling distressed homeowners remains one of the highest-conversion sourcing methods. Foreclosure lists, probate filings, tax-delinquent rolls, and divorce records give you leads. Trained phone skills convert them. A well-placed call to a homeowner facing foreclosure, made at the right time and with the right tone, can generate a deal that no amount of direct mail would have produced.

Pro Tip: Triangulate your target neighborhoods using three data points: absorption rate below 90 days, inventory rising month over month, and a 5% or greater spread between list price and sale price. That combination signals motivated sellers and negotiable terms.

9. Comparing acquisition approaches by investor profile

Different strategies suit different investor types. Here is a direct comparison to help you decide where to focus:

| Strategy | Risk Level | Time Horizon | Best For | Capital Required |

|---|---|---|---|---|

| Buy and hold (Core) | Low | 5 to 10+ years | Stable income, long-term wealth | Moderate to high |

| Fix and flip (Value-Add) | Medium to high | 6 to 12 months | Active operators, rehab experience | Moderate |

| BRRRR | Medium | 12 to 24 months | Capital recycling, scaling | Low to moderate |

| Wholesaling | Low to medium | 30 to 90 days per deal | Low-capital entry, sourcing skill | Very low |

| Tax deed / Opportunistic | High | 1 to 3+ years | Experienced investors, legal resources | Varies |

| 1031 exchange | Medium | Long-term | Portfolio scaling, tax efficiency | High |

A few situational recommendations worth calling out:

- In hot markets with low inventory, off-market cold outreach and wholesaling produce better margins than competing on listed properties.

- In distressed or slow markets, BRRRR and tax deed acquisitions offer the deepest discounts but require the most operational discipline.

- Beginners should start with wholesaling or a single buy-and-hold property to build pattern recognition before moving into higher-complexity strategies.

Explore how acquisition strategy segmentation connects to cold calling execution for each seller type.

My honest take on picking the right approach in 2026

I’ve watched investors lose money not because they picked a bad strategy, but because they picked the right strategy for someone else’s situation. The BRRRR method is genuinely powerful. It is also genuinely brutal if you underwrite the rehab optimistically and get a soft appraisal on the back end. I’ve seen that play out more times than I care to count.

What I’ve learned is that disciplined valuation beats market timing every time. When you use multiple valuation inputs and force yourself to reconcile diverging numbers, you make fewer emotional offers. That discipline is worth more than any market trend or hot neighborhood tip.

I’m also convinced that most investors underinvest in their sourcing skills. The deal you find before anyone else is the deal with the most margin. That means building a real network: title company contacts, foreclosure attorneys, probate specialists, and yes, the ability to have a genuine, productive phone conversation with a homeowner in distress. That last skill is the most underrated one in this business.

The market in 2026 rewards investors who can move fast with conviction. Speed comes from having done the work ahead of time: pre-built valuation models, pre-qualified financing, and a clear sense of which strategy fits the asset in front of you. Stop improvising. Start drilling the fundamentals until they are automatic.

— Dave

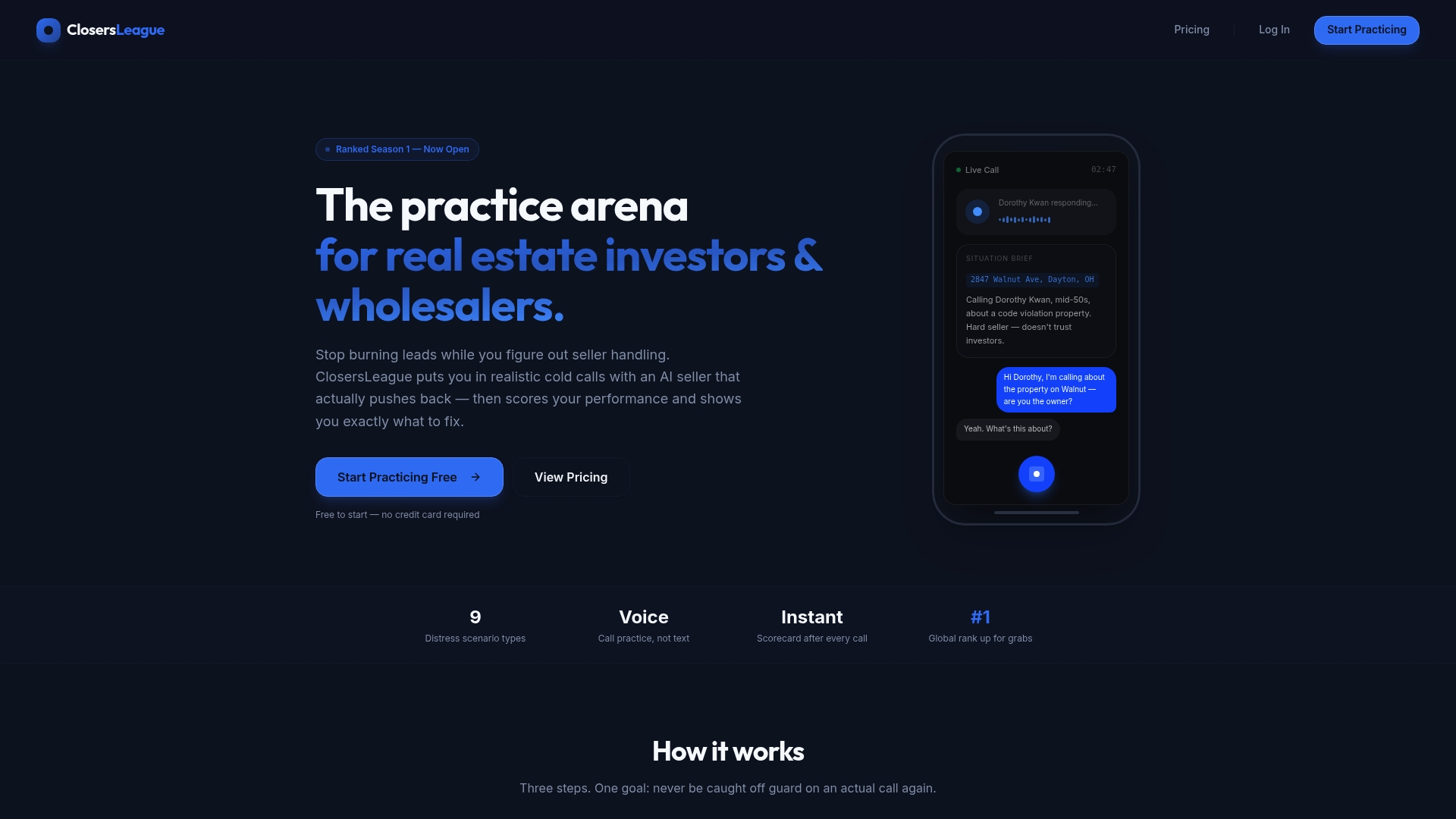

How Closersleague helps you source more deals

Knowing the right acquisition framework is step one. Executing on it through direct seller outreach is where most investors stall. Closersleague is an AI-powered cold calling training platform built specifically for real estate investors and wholesalers who want to sharpen their outreach skills and convert more distressed seller conversations into contracts.

The platform offers AI roleplay for every major seller type, including foreclosure, probate, divorce, and tax-delinquent scenarios. You practice real objections, get scored on your responses, and improve through repetition, not guesswork. If you want to put your property investment strategies into action with better calls and more signed contracts, start practicing today with Closersleague’s AI-powered cold calling practice. Stop winging it. Start drilling.

FAQ

What is the best strategy for acquiring distressed properties?

Wholesaling and BRRRR are the most common approaches for distressed assets because they prioritize deep discounts and speed. Cold calling motivated sellers directly, before properties hit public lists, produces the highest-margin deals for experienced investors.

How important is due diligence in property acquisition?

Due diligence is where most deals succeed or fail. Title reviews, environmental checks, and unpaid tax searches before your offer protect you from inheriting problems that kill your projected returns after closing.

How does the BRRRR strategy work?

BRRRR involves buying a distressed property at a discount, rehabbing it, placing a tenant, and then refinancing to pull your equity back out. The key number is buying at approximately 65 to 70% of ARV minus rehab costs to make the refinance work.

What is a 1031 exchange and when should I use it?

A 1031 exchange lets you defer capital gains taxes by reinvesting sale proceeds into a like-kind replacement property. Use it when scaling a portfolio, but track the 45-day identification window carefully because missing the deadline eliminates the tax benefit entirely.

How do I find off-market deals as a wholesaler?

Use transaction velocity, days on market, and absorption data to identify motivated seller neighborhoods, then reach out directly via cold calling. Foreclosure leads, probate filings, and tax-delinquent property lists are the three most productive sourcing pools for off-market acquisitions.