Most investors assume pre-foreclosure is reserved for hedge funds, institutional buyers, or seasoned pros with deep legal teams. That assumption is wrong, and it’s costing independent investors real money. Pre-foreclosure is one of the most accessible and flexible deal categories available to individual investors and wholesalers who know how to approach a motivated homeowner with empathy and a clear offer. You can negotiate directly, avoid auction bidding wars, and often acquire properties at significant discounts before a bank ever takes control. This article breaks down how pre-foreclosure works, what the numbers look like, where the real risks hide, and how you can build the skills to consistently close these deals.

Table of Contents

- Understanding the pre-foreclosure stage

- Why pre-foreclosure offers unique deal advantages

- Crunching the numbers: Valuation, margin, and deal mechanics

- Mitigating risk and hidden pitfalls in pre-foreclosure

- How market cycles shape pre-foreclosure opportunity

- Why most investors overlook pre-foreclosure (and how to gain an edge)

- Ready to secure more pre-foreclosure deals?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Negotiation flexibility | Pre-foreclosure allows direct owner negotiation for creative and profitable deal structures. |

| Discounted pricing | Homeowner urgency can result in below-market purchase prices compared to auctions. |

| Risk requires diligence | Hidden liens, taxes, and repairs are common, so expert due diligence is non-negotiable. |

| Market timing matters | Shifting inventory and auction competition make pre-foreclosure strategy especially advantageous in 2026. |

Understanding the pre-foreclosure stage

Pre-foreclosure is the period between when a lender files a Notice of Default (NOD) and when the property is sold at a foreclosure auction. During this window, the homeowner still legally owns the property and can sell it, negotiate a payoff, or work out other arrangements. This is your opportunity window as an investor or wholesaler.

The timeline varies significantly by state. Judicial foreclosure states like New York or Florida can take 18 months or longer. Non-judicial states like Texas or California often move much faster, sometimes in 90 to 120 days. Knowing your local foreclosure timeline is not optional. It determines how much time you have to make contact, build rapport, run due diligence, and get a contract signed.

| State type | Typical timeline | Key factor |

|---|---|---|

| Judicial foreclosure | 12 to 24 months | Court approval required |

| Non-judicial foreclosure | 3 to 6 months | Faster trustee process |

| Hybrid states | 6 to 12 months | Lender choice of method |

As a real estate wholesaler basics reference point, understanding what stage a homeowner is in determines the urgency of your outreach and shapes your entire negotiation approach.

Homeowners in pre-foreclosure are often dealing with job loss, divorce, medical debt, or a combination of financial pressures. Their primary motivations are usually debt relief, protecting their credit score, and getting out quickly. They are not looking for the highest possible price. They want a fast, certain solution. That motivation gap is exactly where investors and wholesalers add real value.

“Pre-foreclosure creates a deal discount window because the homeowner is under time pressure while still owning the property.”

The key advantage here is that you are negotiating with a human being, not a loss mitigation department at a bank. That personal dynamic, handled with genuine empathy, is what separates a deal from a dead end.

Common homeowner motivations in pre-foreclosure:

- Avoid the lasting credit damage of a completed foreclosure

- Eliminate or reduce mortgage debt quickly

- Escape ongoing property maintenance they can no longer afford

- Receive a guaranteed, fast close with no open house stress

Why pre-foreclosure offers unique deal advantages

With the basics and timeline established, it’s clear why pre-foreclosure draws savvy investors. Let’s examine what gives it a real competitive edge over REO (bank-owned) properties and auction purchases.

When a bank takes over a property, it introduces bureaucracy, slower timelines, asset managers, and strict “as-is” addendums that leave little room for creative structuring. Pre-foreclosure sidesteps all of that. Investors can negotiate directly with homeowners for more flexible deals before foreclosure finalizes, which opens the door to creative exit strategies that simply aren’t available at auction.

Consider these deal structures that become possible in the pre-foreclosure stage:

- Contract assignment: You lock up the deal under contract and assign your equitable interest to an end buyer for a fee. No rehab required.

- Subject-to financing: You take title “subject to” the existing mortgage, keeping favorable loan terms intact for your buyer or yourself.

- Sale-leaseback agreements: The seller sells the home but leases it back for a defined period, giving them time and you a tenant.

- Partial payoff negotiations: In high-debt situations, you negotiate a discounted payoff with the lender, creating instant equity.

Solid real estate negotiation tactics are what separate investors who close creatively from those who only see one path forward.

Top three reasons experienced investors prefer pre-foreclosures:

- Flexibility: Direct owner negotiation allows terms, timing, and structure that banks never approve.

- Speed: A motivated seller who wants to avoid foreclosure can close in days, not months.

- Margin potential: Buying at a discount before auction competition drives prices up preserves your spread.

Pro Tip: When you call a pre-foreclosure lead, don’t lead with your offer. Lead with a question about their situation. Asking “What’s most important to you in getting out of this property?” before ever quoting a number builds trust and dramatically improves your close rate. Pairing this approach with proven acquisitions strategies gives you a repeatable system.

| Factor | Pre-foreclosure | Auction purchase | REO/Bank-owned |

|---|---|---|---|

| Negotiation flexibility | High | None | Low |

| Competition level | Low to moderate | High | Moderate |

| Speed to close | Fast | Fast (cash required) | Slow |

| Creative deal structures | Yes | No | Rarely |

| Title clarity at purchase | Needs research | Cloudy at times | Usually clean |

Crunching the numbers: Valuation, margin, and deal mechanics

Once you’ve found a potential pre-foreclosure, the real work starts: running the numbers to ensure your deal is as profitable as it looks.

Every serious investor applies a version of the 70% rule as a first filter. The 70% rule formula states: Max Offer = (ARV × 70%) minus Repairs. ARV stands for After Repair Value, which is the property’s projected market value after all improvements are complete. Repairs are your estimated cost to bring the property to that value.

Here’s a quick example. If a property’s ARV is $250,000 and repairs are $40,000:

Max Offer = ($250,000 × 0.70) minus $40,000 = $135,000

That $135,000 is your ceiling. Anything above it erodes your or your buyer’s margin below an acceptable level.

| Variable | Example value | How to calculate |

|---|---|---|

| ARV | $250,000 | Comparable sales within 0.5 miles |

| Repair estimate | $40,000 | Contractor walkthrough or per-sqft estimate |

| 70% of ARV | $175,000 | Multiply ARV by 0.70 |

| Max offer | $135,000 | Subtract repairs from 70% of ARV |

| Wholesale fee | $10,000 to $20,000 | Negotiated with end buyer |

But the 70% rule is just the starting point. You also need to verify:

- Equity position: How much does the homeowner actually owe versus the property value? Negative equity deals require a short sale approval from the lender, which changes your timeline.

- Existing liens: Are there second mortgages, HOA liens, mechanic’s liens, or IRS liens attached to the property? Each one affects your net figure.

- Title status: Is the title clear, or does it carry clouds from prior owners or recording errors?

- Holding and closing costs: Factor in your earnest money risk, title insurance, closing fees, and time cost before finalizing your offer.

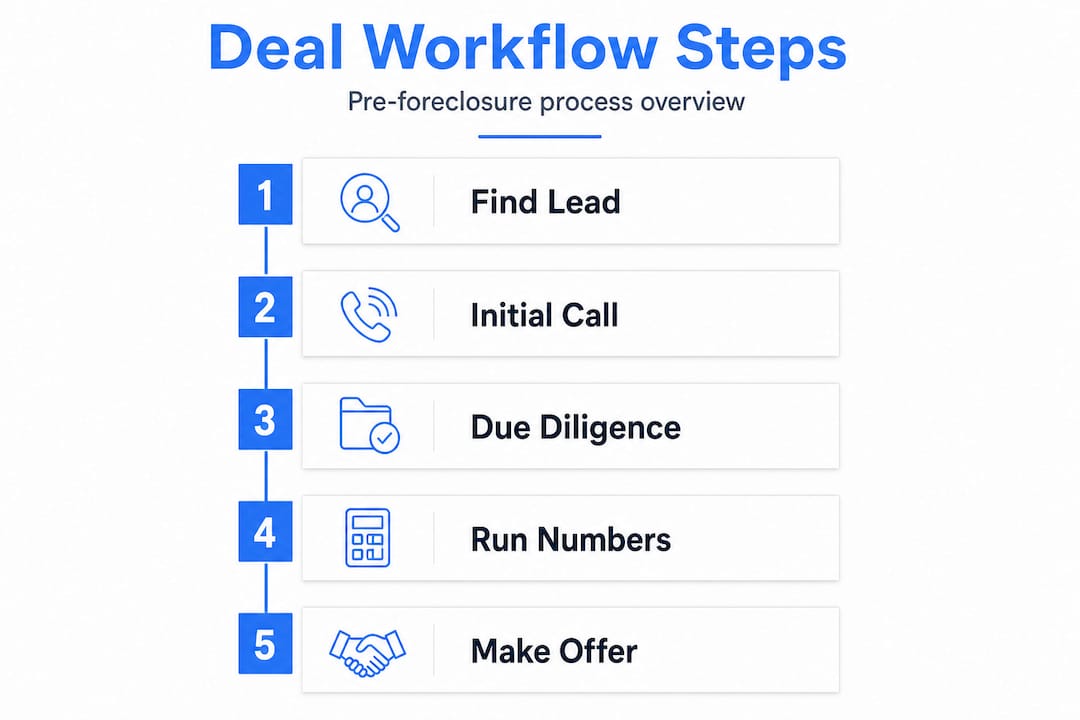

Using a structured investor script workflow to gather property details on your first call saves time and avoids costly surprises. Solid lead qualification methods also help you prioritize which pre-foreclosure leads are worth pursuing versus which ones have too much debt to make a deal work.

Pro Tip: Order a preliminary title report before writing your offer whenever possible. It costs relatively little, usually $50 to $150, and can save you from putting an earnest deposit on a property with $80,000 in IRS liens you didn’t know existed.

Mitigating risk and hidden pitfalls in pre-foreclosure

Margins in pre-foreclosure deals can look great on paper, but here’s where a rookie mistake can turn a fast win into a painful lesson.

Pre-foreclosure properties carry a specific set of risks that don’t always appear during a standard walkthrough. Title defects, unpaid taxes, and undisclosed condition issues can wipe out your spread entirely. Even experienced investors get burned when they skip steps in their due diligence process.

Common pre-foreclosure deal-killers:

- Junior liens: Second mortgages and HELOCs (Home Equity Lines of Credit) that the homeowner forgot to mention or assumed would go away

- IRS tax liens: Federal liens follow the property, not the owner, meaning you inherit them at closing

- HOA delinquencies: Unpaid homeowner association fees can become a lien with legal priority

- Code violations: Open permits or city-issued violations require resolution before sale or transfer

- Deferred maintenance: Roof damage, foundation issues, or mold discovered after contract that exceeds your repair estimate

“Title, unpaid taxes, and undisclosed condition issues can wipe out spread; make comprehensive checks.”

A structured due diligence checklist is not optional on pre-foreclosure deals. It’s your profit protection system. Your process should include a professional title search, a licensed home inspection, a county tax records check, and an HOA status letter before you commit earnest money.

Building strong follow-up strategies also helps you stay in contact with sellers while due diligence runs, especially when title searches take longer than expected. A seller who goes quiet during a two-week title search is not a lost deal. It’s a deal that needs consistent, empathetic follow-up.

Pro Tip: Always ask the homeowner directly, “Are there any other loans, judgments, or unpaid bills tied to this property that you’re aware of?” Most sellers answer honestly when asked plainly, and it gives you a head start on clearing title issues before they kill the deal.

How market cycles shape pre-foreclosure opportunity

Risk management goes hand in hand with market awareness. Let’s see how market cycles can amplify or shrink pre-foreclosure opportunity.

Pre-foreclosure volume is not constant. It rises when unemployment climbs, interest rates spike, or consumer debt reaches unsustainable levels. It contracts during economic booms when homeowners can sell easily on the open market before default deepens. Timing matters, but not in the way most investors think.

Auction activity in Q1 2026 reached 49% of 2020 baseline, with buyers averaging 67.6% of Estimated Recovery Value (ERV). That compression at auction makes pre-foreclosure negotiation even more attractive. When bidders at auction are paying closer to full value, your ability to negotiate privately with a homeowner becomes your primary competitive advantage.

Key market factors to watch in 2026:

- Interest rate movements: Higher rates increase default risk and push more homeowners into distress

- Local unemployment trends: Job loss is the number one trigger for mortgage default

- Foreclosure moratorium expiration: When protection programs end, pipeline volume rises quickly

- Auction clearance rates: When auction clearance drops, pre-foreclosure becomes the more liquid channel for investors

- Days on market for retail listings: When retail listings sit longer, motivated sellers become more open to investor offers

Understanding how to position your offer and pitch in a shifting market is critical. Knowing how to win more wholesale deals in a competitive cycle means adapting your value proposition based on what matters most to sellers right now.

Why most investors overlook pre-foreclosure (and how to gain an edge)

Here’s the uncomfortable truth most real estate educators skip. The majority of investors who “try” pre-foreclosure fail not because of market conditions or deal mechanics. They fail because they avoid the uncomfortable conversation.

Calling a homeowner who is facing foreclosure is emotionally charged. The seller is stressed, often embarrassed, and sometimes hostile. Many investors rather call a random list of absentee owners than sit in that discomfort. And that avoidance is exactly what creates the opportunity for the investors who do show up.

We’ve seen it consistently: investors who approach pre-foreclosure cold calling with a practiced, empathetic script outperform those who wing it. Not because they have better markets or better lists. Because they are prepared to meet the homeowner where they are emotionally, without flinching.

The tactical edge comes from three places. First, run your title research before the call whenever possible. Walking into a conversation knowing the approximate loan balance, lien status, and equity position makes you sound credible and serious. Homeowners in distress can tell immediately whether you know what you’re talking about.

Second, build rapport before making any offer. Your first call should be about understanding, not buying. Ask about their timeline, what they’ve tried so far, and what outcome they’re hoping for. That information shapes an offer they’re more likely to accept.

Third, practice your calls deliberately. Pre-foreclosure homeowners throw objections that feel personal: “I’m not ready,” “My cousin said I should list it,” “I need more than that.” Investors who practice responses to those specific objections before picking up the phone close significantly more deals. Deliberate practice is not optional. It’s the operational edge most of your competition refuses to build.

Ready to secure more pre-foreclosure deals?

Understanding the mechanics of pre-foreclosure is a strong foundation. But knowledge alone doesn’t close deals. Confident, empathetic conversations do.

ClosersLeague is an AI-powered pre-foreclosure cold calling training platform built specifically for real estate investors and wholesalers. You practice realistic calls with distressed homeowners, get scored on your objection handling, and improve with every session. Stop losing deals because you weren’t ready for the tough questions. Try real estate cold calling practice with ClosersLeague and build the conversation skills that turn pre-foreclosure leads into signed contracts.

Frequently asked questions

What makes a pre-foreclosure deal better than buying at auction?

Pre-foreclosure lets you negotiate directly with homeowners for flexible terms and often lower prices, completely avoiding bidding wars and all-cash auction requirements that limit your options.

Can I wholesale a pre-foreclosure property?

Yes, wholesalers frequently assign contracts on pre-foreclosures, but the 70% rule due diligence on liens and repairs is crucial to protect your assignment fee and your buyer’s margin.

Are there risks of hidden liens or unpaid taxes in pre-foreclosure?

Absolutely. Unpaid liens, back taxes, and unclear titles are the most common deal-killers, which is why a professional title search is non-negotiable before committing any earnest money.

How does the real estate market in 2026 impact pre-foreclosure deals?

Auction activity at 49% of 2020 baseline with compressed buyer margins makes private pre-foreclosure negotiation more valuable than ever, especially for investors who can move quickly.

Do all pre-foreclosures let me negotiate directly with the owner?

Most do until the foreclosure sale is completed, but negotiating options and timing depend on the lender and the state-specific foreclosure timeline, so always verify the current stage before assuming you have time.

Recommended

- Qualify real estate leads: proven methods for investors – ClosersLeague Blog

- Top follow-up strategies for investors: boost deal closures – ClosersLeague Blog

- Master Real Estate Negotiation Tactics for Better Deals – ClosersLeague Blog

- Boost Real Estate Deals with a Proven Investor Script Workflow – ClosersLeague Blog