Most investors think buying a property and acquiring a property mean the same thing. They don’t. Real estate acquisitions, in the world of investing and wholesaling, are a deliberate, repeatable process built around finding off-market deals from motivated sellers before the competition ever gets a look. The investors who consistently close deals aren’t just browsing the MLS. They’re working pre-foreclosure lists, calling absentee owners, and structuring contracts that create profit at every exit. This guide breaks down exactly how acquisitions work, how to source the best deals using cold calling, and how to build a pipeline that converts.

Table of Contents

- Defining real estate acquisitions: More than just buying property

- The acquisitions process: Step-by-step for investors and wholesalers

- Finding motivated sellers: Cold calling and off-market deal sourcing

- Legal considerations and risk management for acquisitions

- Comparing residential, wholesale, and commercial acquisitions

- A practitioner’s perspective: What most guides miss about acquisitions

- Practice and scale your acquisitions strategy

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Distressed leads matter | Targeting motivated, off-market sellers unlocks the best acquisition deals for investors and wholesalers. |

| Follow a proven process | A step-by-step acquisitions framework improves deal quality and maximizes results. |

| Benchmarks are your baseline | Cold call conversion and MAO calculations provide realistic expectations and guide actions. |

| Compliance is critical | Understanding legal requirements helps wholesalers avoid costly mistakes and secure deals. |

| Tools boost skills | Practicing your pitch and negotiation strategies leads to more contracts and assignments. |

Defining real estate acquisitions: More than just buying property

When most people hear “real estate acquisition,” they picture a buyer signing paperwork at a title company. But for investors and wholesalers, the word carries a much more specific meaning. Real estate acquisitions involve purchasing or contracting properties, often off-market distressed ones from motivated sellers like pre-foreclosure or absentee owners, to hold, flip, or wholesale for profit. That distinction matters enormously.

A regular home purchase is transactional. An acquisition is strategic. You’re not just looking for any property. You’re targeting sellers whose circumstances create motivation to sell below market value, which creates room for profit.

The types of properties and sellers that investors focus on include:

- Pre-foreclosure homeowners: Facing mortgage default, often needing a fast exit before the bank takes over

- Absentee owners: Own a property but don’t live in it, often dealing with problem tenants or deferred maintenance

- Tax delinquent owners: Owe back property taxes and risk losing the property to a tax lien sale

- Probate properties: Inherited homes that heirs may want to sell quickly to avoid ongoing costs

- Vacant properties: Abandoned or neglected homes that signal distress and seller motivation

Understanding what real estate wholesalers do clarifies how acquisitions differ from retail purchases. A wholesaler doesn’t usually buy a property to own it. They get it under contract at a discounted price and then assign that contract to a cash buyer for a fee. The acquisition skill is what makes or breaks that entire business model.

Analysis and negotiation are central to this process. You need to know the after-repair value (ARV), estimate rehab costs, and determine whether the seller’s situation and price expectations align with your numbers. This wholesaling guide outlines how structuring the deal correctly from the start determines whether the transaction will ever close.

The best acquisitions come from building relationships with distressed sellers before they’re ready to sell, not just chasing leads who are already fielding multiple offers.

With a clear overview in mind, let’s break down the core process that sets acquisitions apart from ordinary property buying.

The acquisitions process: Step-by-step for investors and wholesalers

A structured process separates hobbyists from high-volume operators. The acquisition steps that work in practice follow a clear sequence:

- Market research and define criteria — Pick a geographic farm area and define the property types, price ranges, and seller profiles you’ll target.

- Source leads — Use cold calling, direct mail, and driving for dollars to find distressed properties. Generating cold calling leads consistently is what keeps your pipeline full.

- Analyze deals using the MAO formula — MAO equals ARV multiplied by 70%, minus repairs, minus your wholesale fee. This formula protects your margin.

- Negotiate and get under assignable contract — Once your numbers work, make an offer and use an assignable purchase agreement.

- Due diligence — Verify title, complete inspections, and review any financials or liens.

- Assign the contract or close — Either assign to a cash buyer for a fee or close and add to your portfolio.

- Post-closing responsibilities — Handle tax reporting, update your buyers list, and document lessons for the next deal.

Here’s a quick reference for the MAO formula:

| Variable | Example value |

|---|---|

| After-repair value (ARV) | $200,000 |

| ARV × 70% | $140,000 |

| Minus repairs | $30,000 |

| Minus wholesale fee | $10,000 |

| Maximum Allowable Offer (MAO) | $100,000 |

Review the wholesaler process to see how each step connects across a full deal cycle. For a beginner-friendly breakdown, these wholesaling steps walk through the same framework with additional context.

Pro Tip: Build your cash buyers list before you start chasing deals. If you get a property under contract and have nobody to assign it to, the deal dies. Build demand first, then fill it.

Understanding the full process sets the groundwork for applying these strategies. But how do you actually find motivated sellers to fill your pipeline in the first place?

Finding motivated sellers: Cold calling and off-market deal sourcing

Your deal flow is only as good as your lead sources. Distressed sellers are the highest-value targets for acquisitions because their circumstances create genuine motivation to act. Cold calling is one of the most direct ways to reach them before anyone else does.

The data on cold calling benchmarks is sobering but useful: a 1.7% call-to-appointment rate and a 2.5% lead-to-sale conversion mean you need roughly 5,500 calls to generate 32 qualified leads, 8 contracts, and about 2 completed deals. That’s not discouraging. That’s a system you can plan around.

Best practices for cold calling distressed homeowners:

- Use clean, targeted lists: Pre-foreclosure, tax delinquent, and absentee owner lists give you the highest concentration of motivation

- Qualify fast: Your script should uncover motivation, timeline, and condition within the first 90 seconds

- Follow up same day: The seller who wasn’t ready Monday morning may be ready by Friday afternoon

- Stay in one market: Spreading across too many zip codes kills efficiency. Go deep, not wide

For cold calling tips that apply specifically to distressed homeowner scenarios, your approach needs to lead with empathy, not just numbers. Sellers in distress respond to callers who sound like problem-solvers, not opportunists.

Off-market sourcing is equally critical. Off-market deals found through driving for dollars or public records like probate filings and lien notices yield less competition, but require consistent multi-touch outreach over time. One call rarely closes a deal. Repeated touches build trust.

Using proven investor scripts ensures you’re qualifying sellers efficiently on every call instead of improvising. Consistent scripts also make it easier to track what works and refine your approach.

For hands-on reps, real estate cold calling practice using AI-powered simulations helps you build the muscle memory needed to handle objections, stay calm under pressure, and qualify sellers without sounding robotic. See additional off-market deal sourcing strategies to round out your approach.

Pro Tip: Always use a call script that qualifies both motivation and property condition. Spending 30 minutes with an unmotivated seller is 30 minutes you didn’t spend finding a real deal.

Once you’ve built your list and outreach plan, it’s crucial to understand the legal and compliance nuances that separate success from costly mistakes.

Legal considerations and risk management for acquisitions

Real estate acquisitions carry legal complexity that catches too many beginners off guard. Moving fast without the right structure can turn a promising deal into an expensive problem.

Licensing requirements, deal structures, and TCPA compliance are three areas where investors must be precise:

- Licensing: Some states require a real estate license to wholesale properties. This varies by state and by how the deal is structured. Check your local laws before executing your first contract.

- Assignment vs. double closing: Assigning a contract transfers your rights to a buyer for a fee. A double close involves two separate transactions. Double closes add cost and complexity but protect deal confidentiality when needed.

- TCPA compliance: The Telephone Consumer Protection Act governs cold calling and text outreach. Calling numbers on the Do Not Call registry or using automated dialers without proper consent can result in serious fines.

- Post-closing obligations: Tax reporting, proper transfer of ownership, and filing requirements must be handled correctly after every deal.

- Title issues: Always perform a title search. Liens, judgments, and ownership disputes can kill a deal after you’ve invested significant time.

Cutting corners on compliance doesn’t save time. It creates liability that can set your business back months or years.

For a closer look at wholesaling legal risks, understanding the specific pitfalls around contract language and licensing is essential before you scale. This wholesaling legal guide covers state-specific nuances in detail.

Having addressed both strategy and risk, it’s time to compare acquisition strategies across different real estate niches to see where your approach fits.

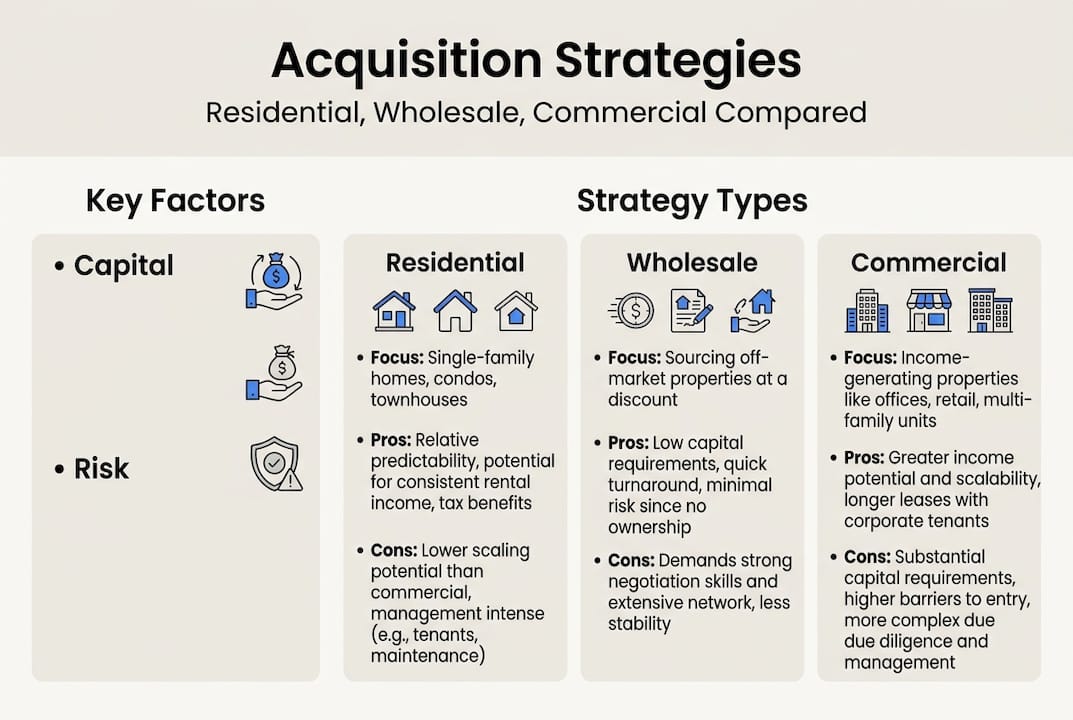

Comparing residential, wholesale, and commercial acquisitions

Not all acquisition strategies are created equal. Your choice should match your capital, network, and risk tolerance. Here’s how the three main approaches stack up:

| Factor | Residential | Wholesaling | Commercial |

|---|---|---|---|

| Capital required | Moderate to high | Low | High |

| Deal source | MLS and off-market | Off-market only | Broker relationships |

| Primary profit method | Appreciation, rent, or flip | Assignment fee | Income analysis and NOI |

| Competition level | High | Moderate to high | Moderate |

| Due diligence focus | Condition and comps | Title and ARV | Financials and tenancy |

| Financing type | Conventional or hard money | Cash buyers | SBA loans, CMBS |

Commercial acquisitions emphasize income analysis and larger financing structures like SBA loans, while wholesaling focuses on quick off-market flips with low capital but high hustle requirements. Residential sits in the middle, often more competitive because more buyers have access to MLS listings.

For those exploring how business acquisitions differ from real estate ones, the financial due diligence models overlap in interesting ways, particularly around valuation and risk assessment.

Now that you’ve seen where acquisition strategies diverge, let’s share an expert perspective on what truly makes top performers stand out.

A practitioner’s perspective: What most guides miss about acquisitions

Most articles on real estate acquisitions focus on the mechanics. The formula, the steps, the legal checklist. That’s all necessary, but it’s not what separates the top performers from everyone else.

In our experience coaching investors and wholesalers, the biggest differentiator is focus. The investors who try to work every market, every seller type, and every exit strategy at once rarely close consistently. The ones who dominate pick one market, learn its distressed seller landscape cold, and work it relentlessly.

Follow-up is the other underrated edge. Same-day follow-up with a warm lead converts at a dramatically higher rate than a callback two days later. Most wholesalers know this but don’t act on it.

And scripts aren’t a crutch. They’re a discipline. Knowing exactly how to qualify motivation and handle objections on cold calling mastery calls gives you consistency that raw volume alone never will. Stop winging it. Start drilling.

Practice and scale your acquisitions strategy

Knowing the framework is step one. Executing it under pressure, with a real seller on the line, is where most investors stall. Skill-building is what closes the gap between understanding acquisitions and actually closing them.

At ClosersLeague, we’ve built an AI-powered practice platform designed specifically for real estate investors and wholesalers. You can practice cold calling across dozens of distressed seller scenarios, from pre-foreclosure to probate, and get scored on your qualification, empathy, and objection handling. Want to sharpen a specific niche? Try the tax delinquent call roleplay to build confidence with one of the most motivated seller profiles in the market. Repetition builds results.

Frequently asked questions

What are the main steps in a real estate acquisition?

Key acquisition steps include market research, lead generation, deal analysis, negotiation, due diligence, getting under contract, and closing or assigning the deal. Each stage builds on the last, and skipping one typically creates problems downstream.

Do I need a license to wholesale properties?

Some states require real estate licenses for wholesaling, so always check your local laws and consult legal counsel before executing deals. Requirements vary significantly depending on how you structure transactions.

How many cold calls does it take to close a deal?

Industry data shows 5,500 calls yield roughly 8 contracts and about 2 completed deals, though your conversion rate will improve significantly with better scripts and consistent follow-up.

What is the MAO formula in real estate?

MAO stands for Maximum Allowable Offer and is calculated as ARV times 70% minus repair costs and your wholesale fee. It’s the ceiling you should never offer above if you want the deal to make financial sense.

Recommended

- Real Estate Cold Calling Practice — AI Roleplay for Every Seller Type | ClosersLeague

- 10 proven cold calling tips for real estate investors – ClosersLeague Blog

- Master Real Estate Lead Generation: Cold Calling Basics – ClosersLeague Blog

- Boost Real Estate Deals with a Proven Investor Script Workflow – ClosersLeague Blog