A distressed homeowner is defined as someone unable to keep up with mortgage payments, property taxes, or basic maintenance costs, often facing foreclosure, short sale, or forced property liquidation as a result. In real estate, the industry term is distressed property owner, and the situation covers far more than just missed payments. Divorce, probate, tax liens, structural damage, and legal judgments all push homeowners into distress. Understanding what causes this situation and what options exist is the first step toward protecting your credit, your equity, and your future.

What is a distressed homeowner and what causes property distress?

A distressed homeowner is someone whose financial, legal, or physical circumstances have made it impossible to sustain normal property ownership. The property itself is then labeled a distressed property, typically selling below market value because of the urgency or condition attached to it. Foreclosure and short sales are the most visible outcomes, but they are rarely the starting point.

Financial, legal, and physical distress are the three pillars that define a distressed property’s challenges. Each pillar creates different complications for both the homeowner and any potential buyer. Financial distress is the most common, but legal or physical issues often complicate sales and financing in ways that catch homeowners off guard.

Here is how the three pillars break down in practice:

| Distress Type | Common Causes | Key Complications |

|---|---|---|

| Financial | Missed mortgage payments, tax liens, HOA arrears | Foreclosure risk, damaged credit, lender intervention |

| Legal | Divorce, probate, lawsuits, title disputes | Clouded title, court delays, forced sale orders |

| Physical | Structural damage, code violations, deferred maintenance | Unfinanceable condition, reduced buyer pool, repair costs |

These categories rarely stay separate. A homeowner going through divorce may simultaneously fall behind on mortgage payments and neglect property maintenance. That overlap accelerates the timeline toward foreclosure and reduces the property’s marketability significantly. Recognizing which type of distress applies to your situation determines which solutions are actually available to you.

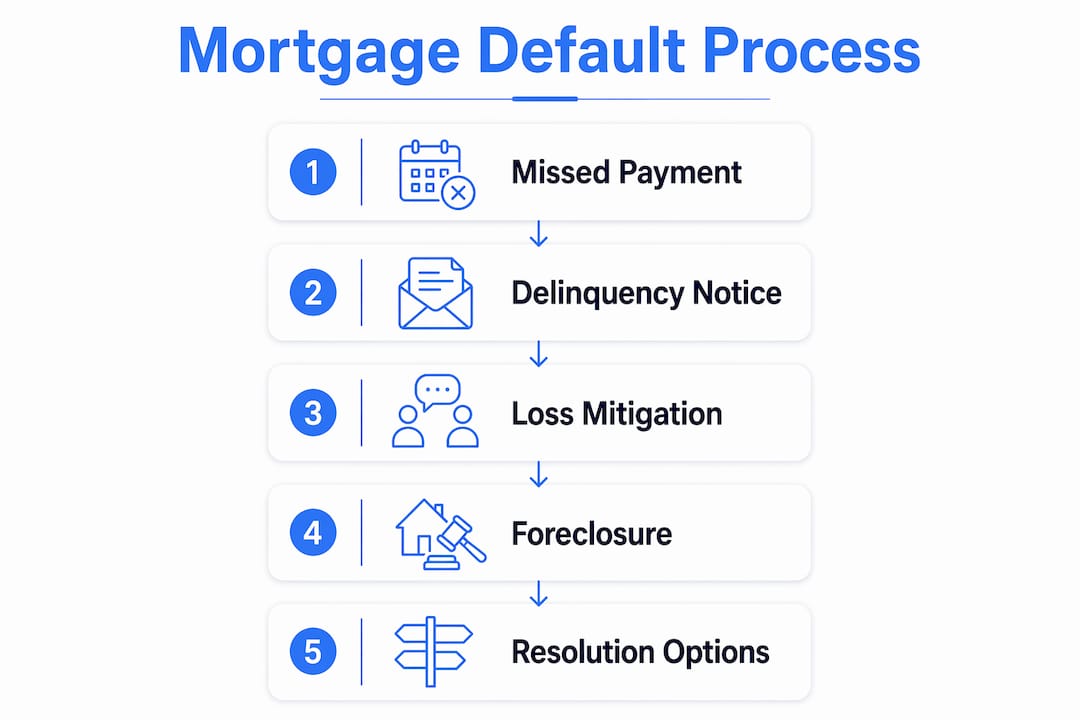

How do lenders recognize and respond to mortgage default?

Lenders begin tracking delinquency the moment a payment is missed, but the formal consequences build gradually over the first few months. A payment 30 days late triggers a credit report entry and a servicer phone call. At 60 days, written notices arrive and late fees accumulate. The real turning point comes between 90 and 120 days.

Foreclosure risk becomes acute after three to four months of consecutive missed payments, triggering formal foreclosure processes. At that stage, the homeowner is classified as seriously delinquent, and the lender’s loss mitigation department takes over the account. After three months of missed payments, lenders send a notice of acceleration, demanding the entire loan balance and initiating pre-foreclosure status. This is the moment most homeowners realize the situation is no longer manageable on their own.

Lenders do have strong financial reasons to avoid foreclosure. Lenders lose money on foreclosure and prefer modifications, forbearance, or short sales as alternatives. This means your servicer is often more willing to negotiate than you expect, especially if you contact them early. Common loss mitigation programs include:

- Forbearance: Temporarily pauses or reduces payments, typically for three to twelve months

- Loan modification: Permanently adjusts the interest rate, loan term, or principal balance

- Repayment plan: Spreads missed payments across future monthly installments

- Payment deferment: Moves overdue amounts to the end of the loan without immediate penalty

Pro Tip: Contact your loan servicer before you miss a payment if possible. Document every call with the date, the representative’s name, and a case number. Early, honest communication opens doors to forbearance and modification that close permanently once foreclosure proceedings begin.

Always ask your servicer directly how each relief option affects your credit score. Credit impacts vary widely by program, and what feels like a lifeline can still leave a mark on your credit report for years.

What options do distressed homeowners have to avoid foreclosure?

Distressed homeowners have more choices than most realize, but the right option depends on whether you want to keep the home or sell it. Timing matters enormously. The earlier you act, the more options remain on the table.

Homeowners in financial distress have options including reinstatement, loan modifications, payment deferment up to 36 months, or short sales. Deferment pauses payments for up to three years; loan modifications adjust rates or terms permanently. These are not favors from the lender. They are structured programs with eligibility requirements, and applying for them requires documentation of your hardship.

The table below compares the most common options available to distressed property owners:

| Option | Best For | Credit Impact | Key Requirement |

|---|---|---|---|

| Reinstatement | Temporary income gap | Minimal if resolved quickly | Lump sum of all missed payments |

| Loan modification | Long-term affordability issue | Moderate, varies by lender | Proof of hardship, income documentation |

| Forbearance | Short-term crisis (job loss, illness) | Low to moderate | Servicer approval, repayment plan agreement |

| Short sale | Underwater mortgage, no equity | Significant but less than foreclosure | Lender approval, buyer offer |

| Deed-in-lieu | No sale possible, no equity | Significant but faster resolution | Lender agreement, clear title |

| Sell with equity | Home worth more than owed | Minimal to none | Positive equity, market-ready condition |

Selling a home with equity during distress can protect your credit and provide funding for your next housing need. Selling before foreclosure stops collection calls and may yield cash for a rental deposit or future purchase. This option is underused because many homeowners assume they have no equity left, when in fact rising home values in many markets mean they do.

Free counseling is available through HUD-approved housing counseling agencies that provide tailored, no-cost foreclosure prevention advice. The Consumer Financial Protection Bureau also accepts mortgage servicer complaints, with responses typically arriving within 15 days. These resources cost nothing and can clarify which programs you actually qualify for before you commit to any path.

How to navigate selling a distressed home and protect yourself

Selling a distressed home requires a different mindset than a standard real estate transaction. Speed, documentation, and awareness of fraud are the three factors that determine whether the process helps or hurts you.

Strategic timing is the single most important variable. Listing before the foreclosure sale date preserves your ability to negotiate, choose your buyer, and potentially walk away with cash. Once the foreclosure auction occurs, those choices disappear entirely. Work with a licensed Realtor who has specific experience with short sales or pre-foreclosure listings, not a generalist who handles distressed sales occasionally.

Pro Tip: Maintain a written communication log with your lender throughout the sale process. Record every conversation, including the date, the representative’s name, and what was agreed. Documenting all communications in writing, keeping records of names and case numbers, is the single most effective way to avoid misunderstandings that derail a short sale approval at the last minute.

Foreclosure rescue scams target distressed homeowners directly, and they are sophisticated. Watch for these warning signs:

- Anyone who asks you to sign over the deed before a sale closes

- Upfront fees for loan modification services that are free through HUD counselors

- Promises of guaranteed foreclosure stops with no lender involvement

- Buyers who pressure you to skip legal review of contracts

For homeowners with FHA loans, FHA delinquency procedures follow a specific timeline and include mandatory loss mitigation steps before foreclosure can proceed. Understanding your loan type changes which protections apply to you. Investors and wholesalers who call distressed homeowners should understand these protections too. Knowing the signs of distressed homeowners and how to approach those conversations with genuine empathy is what separates a helpful investor from one who adds to the problem.

Key takeaways

A distressed homeowner facing foreclosure or financial hardship has more options than most realize, but acting before the 90-day delinquency threshold is the single most important factor in preserving those choices.

| Point | Details |

|---|---|

| Three pillars of distress | Financial, legal, and physical distress each create different complications and require different solutions. |

| 90-day threshold | Foreclosure risk becomes acute after three to four months of missed payments, making early action critical. |

| Lenders prefer alternatives | Lenders lose money on foreclosure and actively offer forbearance, modification, and short sale options. |

| Free counseling exists | HUD-approved agencies provide no-cost foreclosure prevention advice tailored to your specific situation. |

| Equity changes everything | Homeowners with positive equity can sell before foreclosure, protect their credit, and retain cash proceeds. |

What I’ve learned from watching homeowners wait too long

The pattern I see most often is this: a homeowner misses one payment, tells themselves they will catch up next month, and then misses two more. By month three, they are in pre-foreclosure with far fewer options than they had 90 days earlier. Many homeowners wait too long before contacting the lender, losing access to early loss mitigation programs that could have resolved the situation cleanly.

The emotional toll of financial distress is real, and it makes people avoid the very conversations that would help them. Shame, fear of judgment, and the hope that things will improve on their own are powerful forces. But lenders are not looking to punish you. They are looking to recover money, and a modification or short sale does that more efficiently than a foreclosure auction.

What I find encouraging is that the resources genuinely exist. HUD counselors, legal aid organizations, and experienced Realtors who specialize in distressed sales can all provide real help at little or no cost. The homeowners who come out of distress in the best shape are not the ones with the most money. They are the ones who picked up the phone early, asked direct questions, and kept records of every answer.

If you are an investor or wholesaler working with distressed homeowners, understanding this emotional context is not optional. It is the foundation of every productive conversation. Qualifying a distressed property lead starts with recognizing what the homeowner is actually going through, not just what the property is worth.

— Dave

How ClosersLeague helps real estate professionals connect with distressed homeowners

Real estate investors and wholesalers who work with distressed homeowners know that the conversation itself is the hardest part. You need to ask the right questions, handle objections with empathy, and qualify the lead without making the homeowner feel pressured.

ClosersLeague is an AI-powered cold calling practice platform built specifically for investors and wholesalers who call foreclosure, probate, divorce, and tax-delinquent leads. You practice live roleplay scenarios, get scored on your responses, and build the muscle memory to handle real conversations with confidence. Stop winging it. Start drilling. ClosersLeague gives you the reps you need before the call that counts.

FAQ

What is a distressed homeowner?

A distressed homeowner is someone unable to meet mortgage payments, property tax obligations, or maintenance costs, often facing foreclosure, short sale, or forced liquidation of their property.

What are the signs of a distressed homeowner?

Common signs include missed mortgage payments, deferred property maintenance, tax liens, pending divorce or probate proceedings, and properties listed significantly below market value.

How long before a missed payment leads to foreclosure?

Foreclosure risk becomes acute after 90 to 120 days of missed payments. At that point, lenders issue a notice of acceleration and initiate pre-foreclosure proceedings.

What free help is available for distressed homeowners?

HUD-approved housing counseling agencies provide no-cost foreclosure prevention advice. The Consumer Financial Protection Bureau also accepts mortgage servicer complaints and typically delivers responses within 15 days.

Is selling better than foreclosure for a distressed homeowner?

Selling before foreclosure, especially when equity exists, protects your credit score, stops collection activity, and may provide cash for your next housing situation. Foreclosure causes significantly more long-term credit damage.