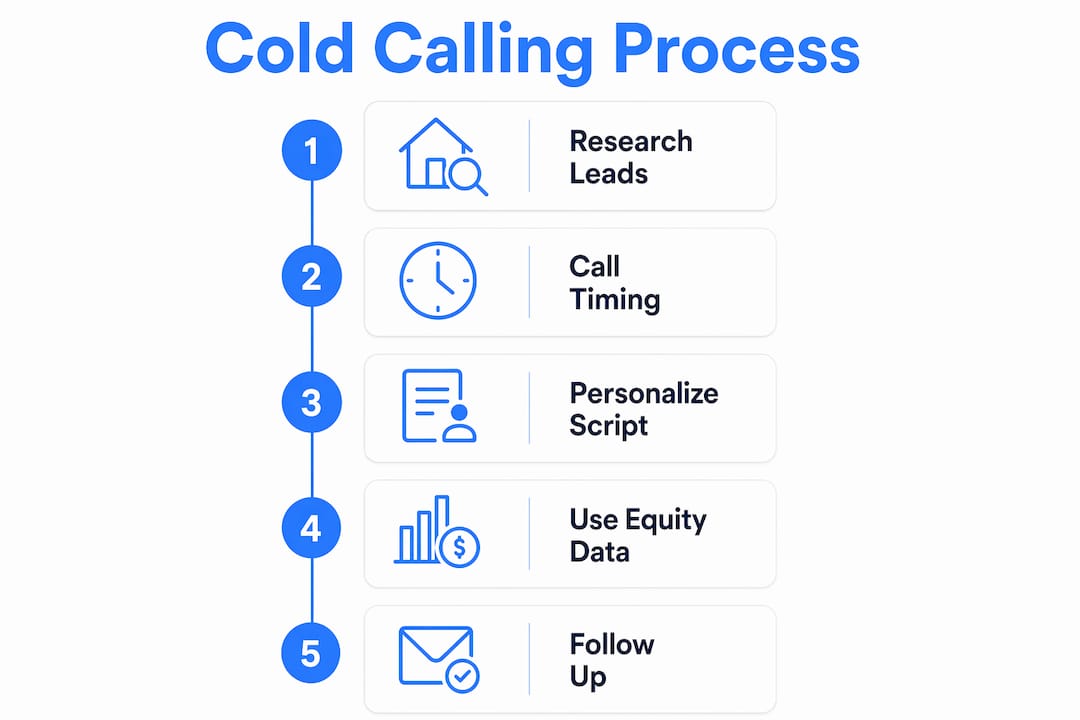

Cold calling foreclosure properties is a direct outreach strategy where real estate investors and wholesalers contact homeowners who have received a Notice of Default (NOD) before the bank takes the property. The industry term for this work is pre-foreclosure outreach, and it sits at the intersection of timing, empathy, and data. Done right, it connects you with motivated sellers before your competition even knows the lead exists. This guide covers the full method: when to call, how to script your approach, how to use equity data, and how to follow up until you close.

Cold calling foreclosure properties guide: when is the best time to call?

The golden window after an NOD filing is 14–45 days. That is when homeowners are anxious enough to talk but still have time to act. Call too early and they are in denial. Call too late and they are either in attorney mode or the property has already been listed.

Foreclosure timelines vary significantly by state. Non-judicial states like Texas and California typically run 60–90 days from NOD to auction. Judicial states like Florida and New York can stretch 180 days or more. That longer window gives you more attempts, but it also means more competition from other investors who are working the same list.

Here is what the timing breakdown looks like in practice:

- Days 1–14 post-NOD: Homeowner is processing the notice. Most are not ready to talk. Skip this window.

- Days 14–45 post-NOD: The sweet spot. Anxiety is real, options feel limited, and they are open to solutions.

- Days 45–90 post-NOD: Still workable in non-judicial states, but urgency shifts to the homeowner’s favor. You need a strong value proposition fast.

- Beyond 90 days: In judicial states, you still have time. In non-judicial states, the auction clock is loud.

Pro Tip: Pull your NOD list weekly, not monthly. Leads that are 14 days old on a weekly pull are still warm. Leads that are 45 days old on a monthly pull are already cold.

Owner-occupied properties and absentee landlord properties require different timing instincts. Occupant homes need more empathy and urgency calibration. An absentee landlord in foreclosure is often more transactional and less emotionally attached to the property. Adjust your opening accordingly.

How to personalize your cold calling script for foreclosure leads

The first rule of foreclosure cold calling scripts is to never say “foreclosure” in your opening line. The word carries stigma and triggers an immediate defensive response. Neutral language reduces hang-ups and keeps the conversation alive long enough to build rapport.

Use phrases like “a notice you may have received recently” or “a challenging situation with your property.” These phrases acknowledge the reality without labeling it. The homeowner knows what you mean. You do not need to say it outright to be understood.

Your script structure should follow this sequence:

- Introduction: State your name, your company, and your purpose in one sentence. “Hi, my name is [Name] with [Company]. I work with homeowners in [City] who are dealing with difficult property situations.”

- Empathy bridge: Acknowledge their situation without assuming. “I understand this may be a stressful time, and I just wanted to reach out to see if there’s anything I can help with.”

- Permission ask: Do not pitch. Ask if they are open to a brief conversation. “Would you be open to a quick 10-minute call this week to explore your options?”

- Two-option close: If they hesitate, give them two choices instead of an open question. A two-option close like “Would Tuesday or Thursday work better for a brief chat?” significantly increases appointment rates versus asking “When are you free?”

“The goal of your first call is not to make an offer. The goal is to earn the right to a second conversation.” This mindset shift changes everything about how you sound on the phone.

The initial call’s purpose is to secure permission for follow-up, not to close a deal. Investors who try to close on the first call almost always fail. Investors who focus on building trust and scheduling the next contact convert at a much higher rate.

Pro Tip: Practice your opening 30 seconds until it sounds completely natural. That first half-minute determines whether the homeowner stays on the line or hangs up. Use AI roleplay tools to drill it before you dial real leads.

Occupancy status also shapes your script. An owner-occupant is emotionally tied to the home. Your language should reflect that. An absentee landlord is more concerned with financial exposure. Customize your approach based on occupancy to connect faster and waste fewer calls.

How to use equity data to tailor your offers and talk strategy

Pre-call equity research is not optional. Knowing the equity tier before you dial tells you what kind of offer is even possible and saves you from wasting calls on deals that cannot work.

Equity analysis means calculating the homeowner’s loan-to-value ratio against current market value. Tools like EquityTier and Deal Analyzer pull this data before you make a single call. Without it, you are guessing. With it, you know whether to pitch a cash offer, a creative structure, or a referral to a realtor.

| Equity Situation | What It Means | Best Offer Strategy |

|---|---|---|

| High equity (30%+ above loan) | Homeowner has room to sell below market and still walk away with cash | Standard cash offer or traditional sale referral |

| Low equity (under 10%) | Thin margin, limited options | Negotiate hard on price, explore short sale |

| No equity or underwater | Loan balance exceeds property value | Subject-to deal, short sale, or loan assumption |

For no-equity cases, a generic cash offer is not just unhelpful. It is insulting. No-equity owners need creative structures like subject-to deals, where you take over the existing mortgage payments. This approach solves their problem without requiring them to bring cash to the table. Homeowners in this position are often relieved to hear there is a path forward that does not require a check they do not have.

Loan modifications are another option homeowners often pursue. Loan mods are approved less than 40% of the time and take 3–6 months to process. That makes you, the investor, a credible and faster alternative. Knowing this statistic lets you position yourself honestly without being predatory. You are not replacing their bank. You are offering a solution the bank often cannot.

Pro Tip: Run your equity analysis before every call, not after. Investors who skip this step waste time pitching deals that cannot close and burn rapport with homeowners who sense the offer is not realistic.

Understanding why homeowners sell during pre-foreclosure also sharpens your talk strategy. Sellers in this window are not just motivated by money. They are motivated by relief, dignity, and speed. Your offer needs to address all three.

What is the optimal follow-up cadence after the initial cold call?

Most deals do not close on the first call. Successful conversions typically happen between the 3rd and 8th contact, with consistent follow-up over 30 or more days. Investors who stop after one or two attempts leave the majority of their potential deals on the table.

The recommended follow-up schedule looks like this:

- Day 1: Initial cold call. Goal is rapport and permission for follow-up.

- Day 3: Second call or text. Reference your previous conversation by name and detail.

- Day 7: Third call plus a handwritten or direct mail piece. Physical mail reinforces your credibility.

- Day 14: Fourth call. By now, the homeowner’s situation has likely changed. Urgency is higher.

- Day 21–30: Continue with texts, voicemails, and mail. Do not go silent.

Multi-channel outreach consistently outperforms single-channel cold calling. Combining calls with texts and direct mail creates multiple touchpoints that build name recognition. By the time a homeowner is ready to talk, your name is the one they remember.

Logging every call with detailed notes is what separates professional investors from amateurs. Note the homeowner’s tone, any personal details they shared, and the exact reason they gave for not being ready. Use those notes on your next call to show you were listening. That level of personalization builds trust faster than any script.

Pro Tip: Set a calendar reminder for every follow-up before you hang up the phone. Do not rely on memory. Investors who log and schedule in real time follow through. Investors who plan to “do it later” lose the deal.

Persistence is not the same as pressure. Calling every day is pressure. Calling on a structured schedule with genuine value in each touchpoint is persistence. Homeowners in foreclosure are dealing with stress from every direction. The investor who shows up consistently, respectfully, and with real solutions is the one who earns the conversation when the homeowner is finally ready to move.

Key takeaways

Cold calling foreclosure property owners requires precise timing, empathetic scripting, equity-informed offers, and structured follow-up across multiple channels to convert motivated sellers.

| Point | Details |

|---|---|

| Call in the 14–45 day window | Contact homeowners within 14–45 days of the NOD filing for the highest response rate. |

| Avoid the word “foreclosure” | Use neutral language like “a notice you may have received” to keep homeowners on the line. |

| Run equity research before every call | Use tools like EquityTier and Deal Analyzer to match your offer strategy to the homeowner’s actual situation. |

| Follow up 3–8 times across channels | Most conversions happen between the 3rd and 8th contact using calls, texts, and direct mail. |

| Secure follow-up, not an immediate close | The first call goal is earning the next conversation, not making an offer. |

What I have learned from years of foreclosure cold calling

The biggest mistake I see investors make is treating foreclosure calls like a numbers game. They dial fast, pitch hard, and move on when they get a no. That approach burns leads and burns bridges. Homeowners in pre-foreclosure are not just a list. They are people in one of the most stressful situations of their lives.

Empathy is not a soft skill in this business. It is a conversion tool. The investors I have watched close the most deals are the ones who slow down, listen more than they talk, and genuinely try to understand what the homeowner needs. That does not mean you avoid making offers. It means your offer lands in a context where the homeowner trusts you enough to consider it.

The other mistake I see constantly is ignoring equity data. Investors pull a list, start dialing, and pitch the same cash offer to every homeowner regardless of their loan balance. That is how you waste 40 calls and close zero deals. Run the equity analysis first. Know what you are walking into before you say hello.

Script rigidity is the third pitfall. A script is a framework, not a transcript. If you are reading word for word, the homeowner hears it. Practice your script until you can have a real conversation within its structure. The foreclosure cold call roleplay work I recommend most is the kind that throws objections at you in real time, because that is exactly what homeowners do.

The investors who win in this space are not the loudest or the fastest. They are the most prepared, the most consistent, and the most human.

— Dave

Practice your foreclosure calls before you dial real leads

Cold calling distressed homeowners is a skill. Like any skill, it gets sharper with deliberate practice, not just repetition.

ClosersLeague is an AI-powered cold calling training platform built specifically for real estate investors and wholesalers. You can practice pre-foreclosure cold calling scenarios with an AI that responds like a real homeowner, throws real objections, and scores your performance. You will build confidence, refine your script, and handle objections before they cost you a live deal. If you want to sharpen every seller type, the full AI roleplay practice platform covers foreclosure, probate, divorce, and more. Stop winging it. Start drilling.

FAQ

When should you first call a foreclosure property owner?

The best time to call is 14–45 days after the Notice of Default is filed. This window gives homeowners enough time to process the notice while still leaving room to act before the auction.

Should you say “foreclosure” on a cold call?

No. Using the word “foreclosure” early in a call increases hang-ups. Use neutral phrases like “a notice you may have received” to keep the conversation open.

How many times should you follow up with a foreclosure lead?

Follow up at least 3–8 times across calls, texts, and direct mail over 30 or more days. Most conversions happen after the third contact, not the first.

What is a subject-to deal and when does it apply?

A subject-to deal means you take over the homeowner’s existing mortgage payments instead of paying off the loan. It applies when a homeowner has little or no equity and cannot sell through a traditional cash offer.

How does equity data change your offer strategy?

Equity data tells you whether a cash offer is feasible or whether you need a creative structure like a subject-to deal. Calling without equity research leads to offers that do not fit the homeowner’s situation and waste everyone’s time.