Types of foreclosure sellers are categories of property owners compelled to sell due to financial distress, life events, or external deadlines that remove the luxury of waiting. The industry term for these owners is “motivated sellers,” and recognizing which category you fall into directly shapes your sale options, timeline, and credit outcome. External deadlines triggered by foreclosure proceedings differentiate these sellers from typical homeowners who can afford to wait for the right offer. Whether you received a Notice of Default last week or inherited a property with back taxes, your seller category determines what moves are still available to you.

1. types of foreclosure sellers: the core categories

The types of foreclosure sellers break down into six distinct groups, each driven by different pressures and operating under different timelines. Pre-foreclosure homeowners, auction sellers, bank-owned property sellers, probate sellers, divorce-related sellers, and landlord burnout sellers all share one trait: urgency. That urgency is what separates them from a traditional seller who lists on the MLS and waits 90 days for the right buyer. Understanding which category applies to you is the first step toward choosing a sale strategy that protects your credit and puts money in your pocket.

2. pre-foreclosure sellers: still in control

Pre-foreclosure sellers are homeowners who have received a Notice of Default from their lender but still hold legal title to the property. This is the most time-sensitive and most misunderstood seller category. Many homeowners in this position incorrectly believe they have already lost the right to sell, but legal ownership remains with the homeowner until the foreclosure auction is completed.

The Notice of Default typically arrives 90–120 days before the scheduled auction. That window is real and usable. Your options during this period include:

- Traditional sale: List with an agent if time allows. This works best in the early stages of the pre-foreclosure window.

- Cash sale: Cash buyers close in 3–14 days, which makes them the most practical option for sellers in late-stage pre-foreclosure.

- Short sale: If you owe more than the home is worth, a short sale requires lender approval and typically takes 60–180 days. It is a viable option but not a fast one.

Pre-foreclosure sellers often accept 10–30% discounts below market value to close quickly and avoid the auction. That discount buys speed, certainty, and a significantly better credit outcome than a completed foreclosure.

Pro Tip: Contact a cash buyer the moment you receive a Notice of Default. Every day you wait narrows your options. A fast cash offer accepted early in the pre-foreclosure window gives you the most negotiating room and the best chance of preserving your credit score.

3. foreclosure auction sellers: when time runs out

Auction sellers are homeowners whose properties have reached the public foreclosure sale. At this stage, the homeowner loses title the moment the auction gavel falls. The credit damage from a completed foreclosure is severe and long-lasting, which is why reaching this stage is the outcome every pre-foreclosure seller should work to avoid.

Foreclosure timelines range from 3–18 months depending on the state and whether the foreclosure is judicial or non-judicial. States like New York and New Jersey have judicial processes that can stretch past a year, while states like Texas and Georgia move much faster. That timeline gap matters because it determines how much runway you have to sell before the auction.

One fact most homeowners do not know: lenders often prefer a voluntary sale over completing the auction. Showing a lender a signed purchase agreement or active listing can trigger an auction postponement. Lenders carry real costs when they take a property to auction and then manage it as REO inventory, so they have a financial reason to cooperate with a seller who is actively working toward a closing.

4. bank-owned (REO) sellers: institutional motivation

Bank-owned properties, formally called Real Estate Owned or REO, are homes the lender acquired after a failed foreclosure auction. The bank is now the seller, and its motivation is straightforward: reduce inventory, cut holding costs, and move the asset off its books. Institutional REO sellers price below market to reduce administrative burden and fees associated with managing vacant properties.

REO sales differ from owner-led sales in several important ways:

| Factor | REO Bank Seller | Pre-Foreclosure Owner |

|---|---|---|

| Motivation | Inventory reduction, cost control | Credit preservation, debt relief |

| Negotiation style | Formal, committee-driven | Personal, emotionally driven |

| Property condition | Sold as-is, often vacant | May be occupied, variable condition |

| Closing timeline | 30–60 days typical | 7–60 days depending on method |

| Price flexibility | Moderate discounts | 10–30% below market common |

For buyers, REO properties offer predictable title and clear ownership. For the original homeowner, reaching REO status means the foreclosure is complete and the credit damage is already done. The lesson here is that the REO stage is what you are trying to avoid by acting during pre-foreclosure.

5. probate and inherited property sellers

Probate sellers are heirs or estate administrators who inherit a property and need to liquidate it, often quickly. The property may carry a mortgage, back taxes, or deferred maintenance that makes holding it financially impractical. Life events like inheritance create motivated sellers with an urgent need to sell before financial hardship compounds.

These sellers are not always in foreclosure at the time of sale, but they frequently become foreclosure-adjacent when the inherited mortgage goes unpaid during the probate process. Probate can take 6–12 months in most states, and a property sitting vacant during that period accumulates costs fast. Heirs who act early by engaging a cash buyer or real estate attorney can often close before the lender files a Notice of Default.

The emotional component of probate sales is real. Sellers are grieving while simultaneously managing a legal and financial process they may have never encountered before. That combination of emotional weight and financial urgency makes probate sellers one of the most motivated categories in the distressed seller spectrum.

Pro Tip: If you inherited a property with an existing mortgage, call the lender immediately to notify them of the owner’s death. Most lenders will grant a short grace period before filing default notices, but only if you communicate proactively. Silence accelerates the foreclosure clock.

6. divorce-related sellers: urgency from life change

Divorce-related sellers are co-owners who must sell a shared property as part of a legal settlement or because neither party can afford the mortgage alone. The court often sets a hard deadline for the sale, which creates the same kind of non-negotiable urgency as a foreclosure auction date. Divorce and job relocation consistently rank among the top motivators for sellers who accept discounts in exchange for fast closings.

The complication with divorce sales is that both parties must agree on the sale terms, the buyer, and the price. When communication between the parties breaks down, the sale stalls, the mortgage goes unpaid, and a pre-foreclosure situation develops. Sellers in this category benefit most from a single-decision-point sale structure, which is exactly what a cash buyer or wholesaler offers.

7. job relocation sellers

Job relocation sellers face a hard geographic deadline. A new job starts in six weeks in another city, and the house needs to sell before then. These sellers are not necessarily in financial distress at the moment of sale, but they become distressed quickly if the property does not sell before they relocate. Carrying two housing costs simultaneously is the financial pressure that drives this category.

Relocation sellers typically accept modest discounts, around 5–15% below market, in exchange for a guaranteed closing date. They prioritize certainty over price. A cash offer with a flexible closing date is often more attractive to a relocation seller than a higher offer contingent on financing approval.

8. tax-delinquent property sellers

Tax-delinquent sellers own properties with unpaid property taxes that have triggered a tax lien or are approaching a tax sale. Unlike mortgage foreclosure, tax foreclosure moves on a separate government timeline and can result in the loss of the property for a fraction of its value. Sellers in this category often do not realize how close they are to losing the property entirely until the tax sale notice arrives.

The good news is that tax liens are payable at closing from sale proceeds, which means a cash sale can resolve the delinquency and still put money in the seller’s pocket. The key is acting before the tax sale date, not after.

9. tired landlord and absentee owner sellers

Tired landlords are property owners who are done managing rental properties. Vacancies, non-paying tenants, code violations, and deferred maintenance have made the property a liability rather than an asset. Motivated sellers often stem from landlord burnout and absentee ownership, not just financial distress.

These sellers frequently accept below-market prices because they want the problem gone. They are not always in foreclosure, but many are heading there due to missed mortgage payments caused by rental income loss. A landlord with three vacant units and a mortgage payment due is a seller with real urgency, even if no Notice of Default has been filed yet.

Key takeaways

Understanding the different foreclosure seller categories is the single most important factor in choosing the right sale strategy before the auction clock runs out.

| Point | Details |

|---|---|

| Pre-foreclosure is your best window | You retain sale rights until the auction completes, so act the moment you receive a Notice of Default. |

| Cash sales close fastest | Cash buyers can close in 3–14 days, making them the most practical option for late-stage pre-foreclosure sellers. |

| Lenders prefer voluntary sales | Showing a lender a signed purchase agreement can delay the auction and create more time to close. |

| Life events create equal urgency | Divorce, probate, and job relocation produce the same seller urgency as financial distress. |

| REO status means the damage is done | Bank-owned properties signal a completed foreclosure. Avoiding this stage protects your credit for years. |

What i’ve learned watching sellers wait too long

I have seen every seller type described in this article, and the pattern that costs homeowners the most is not making the wrong decision. It is making no decision at all. Sellers in pre-foreclosure receive the Notice of Default and freeze. They assume the situation is too complicated, or they hope the lender will work something out. Meanwhile, the auction date moves closer.

The sellers who come out ahead are the ones who treat the Notice of Default like a starting gun, not a death sentence. They call a cash buyer the same week. They contact their lender with a purchase agreement in hand. They understand that proactive communication with lenders can unlock auction delays that most homeowners assume are impossible.

One thing I want to push back on is the idea that accepting a discount is always a loss. When you factor in the credit damage from a completed foreclosure, the legal fees, the stress, and the years it takes to rebuild your borrowing power, a 15% discount on a fast cash sale is often the financially superior outcome. The sellers who understand this math act faster and land better.

The other thing worth saying plainly: life events like divorce and probate are not lesser forms of distress. They carry the same financial urgency as a missed mortgage payment, and they deserve the same level of urgency in your response. If you are sitting on an inherited property with an unpaid mortgage, you are already in the foreclosure seller category whether you feel like it or not.

— Dave

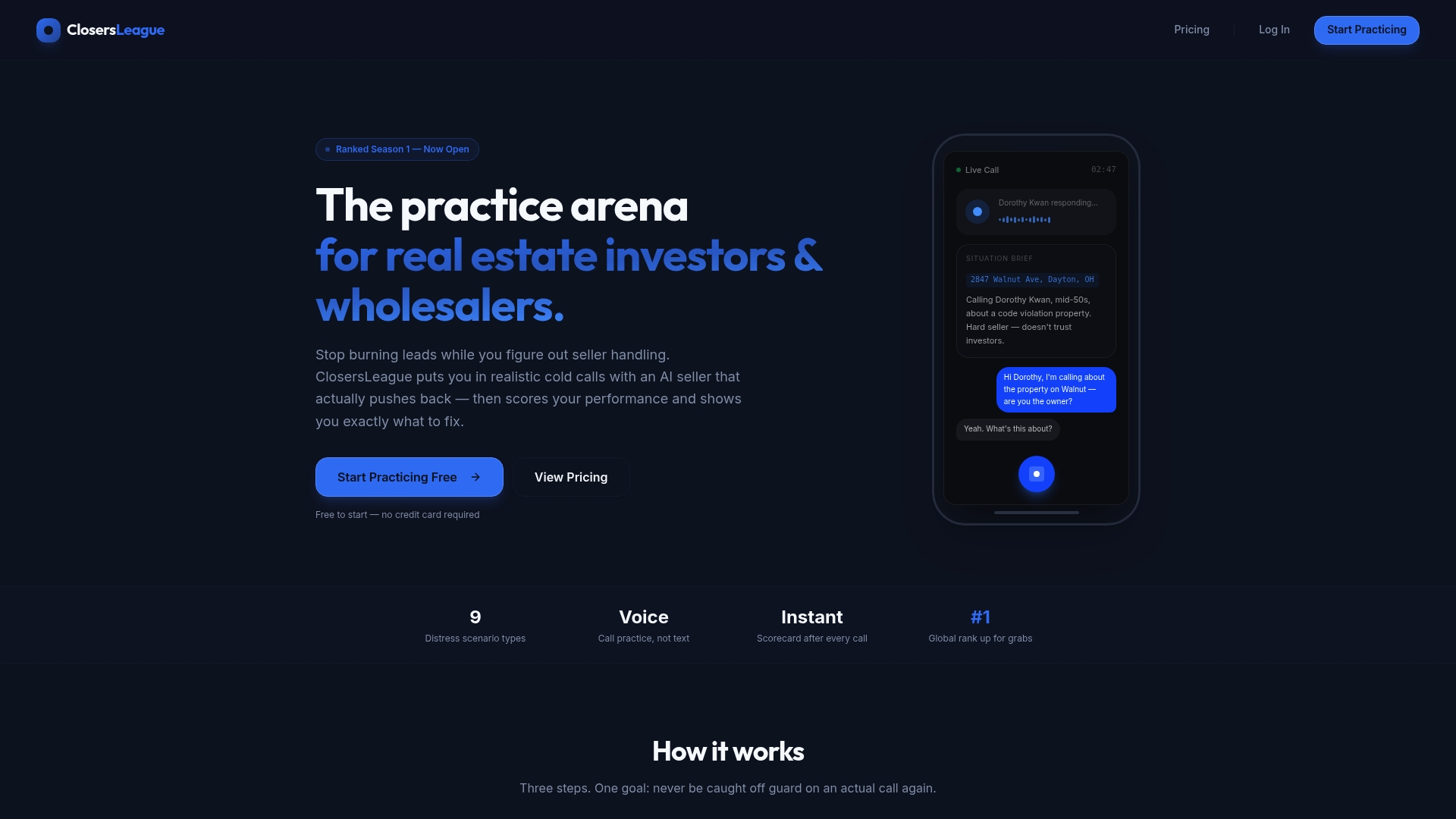

Practice the calls that convert foreclosure sellers

Knowing the different foreclosure seller categories is one thing. Knowing what to say when one of them picks up the phone is another skill entirely.

ClosersLeague is an AI-powered cold calling training platform built specifically for real estate investors and wholesalers who work with distressed sellers. The platform lets you practice cold calling scripts for every seller type covered in this article, from pre-foreclosure homeowners to tired landlords, with real-time AI feedback on your tone, objection handling, and closing approach. Stop guessing how a conversation will go. Start drilling the exact scenarios you will face on your next call. Visit ClosersLeague and run your first AI roleplay session today.

FAQ

What is a pre-foreclosure seller?

A pre-foreclosure seller is a homeowner who has received a Notice of Default from their lender but still holds legal title to the property. They can sell at any point before the foreclosure auction is completed.

How fast can a foreclosure seller close a sale?

Cash sales close in as few as 3–14 days, making them the fastest option for sellers facing an upcoming auction date. Traditional sales and short sales take significantly longer, often 30–180 days.

Do lenders ever delay foreclosure auctions for sellers?

Yes. Lenders often postpone auctions when a seller presents a signed purchase agreement or active listing, since completing an auction and managing REO inventory costs the lender more than a voluntary sale.

What is the difference between a short sale and a cash sale?

A short sale requires lender approval to accept less than the mortgage balance and typically takes 60–180 days. A cash sale closes on the open market without lender approval and can close in under two weeks.

Who sells foreclosed properties after the auction?

After a foreclosure auction, the lender takes ownership and becomes the seller of a bank-owned or REO property. These institutional sellers price below market to reduce holding costs and move the asset off their books.