A distressed seller is a homeowner compelled to sell their property quickly due to urgent financial or personal hardship, typically at a price well below market value. The industry term for this situation is a “distress sale,” and it covers a wide range of circumstances from foreclosure and divorce to bankruptcy and medical debt. Distressed sellers often accept 20–40% below comparable market value to resolve their crisis fast. That discount reflects urgency, not necessarily a problem with the property itself. If you are facing one of these situations, understanding how distress sales work gives you real options.

What is a distressed seller, and what causes seller distress?

A distressed seller is defined as a property owner whose personal or financial circumstances force a faster sale than the open market typically allows. The pressure comes from outside the real estate transaction itself. Distress is linked to the owner’s finances, not the home’s intrinsic quality. Many distressed properties sit in desirable neighborhoods and are structurally sound.

The triggers vary widely, but they share one common thread: the seller cannot afford to wait. Common triggers include foreclosure risk, bankruptcy, divorce, medical debt, and severe property disrepair. Each of these creates a different kind of pressure with different legal and financial consequences.

Seller distress generally falls into two categories:

- Financial distress: Missed mortgage payments, IRS tax liens, bankruptcy filings, or medical bills that exceed available cash. The home becomes the fastest source of liquidity.

- Situational distress: Life events like divorce, job relocation, probate, or an inherited property the owner cannot maintain. The urgency is real but not always tied to debt.

- Property condition distress: Code violations, severe structural damage, or deferred maintenance that makes the home difficult to sell through traditional channels.

- Legal distress: Court orders, estate settlements, or judgments that require the property to be liquidated within a specific timeframe.

- Combination distress: Many sellers face two or more of these at once. A divorce that triggers missed payments, for example, compounds the urgency significantly.

Recognizing which type applies to your situation shapes every decision you make next, from which sale route to choose to how much time you realistically have.

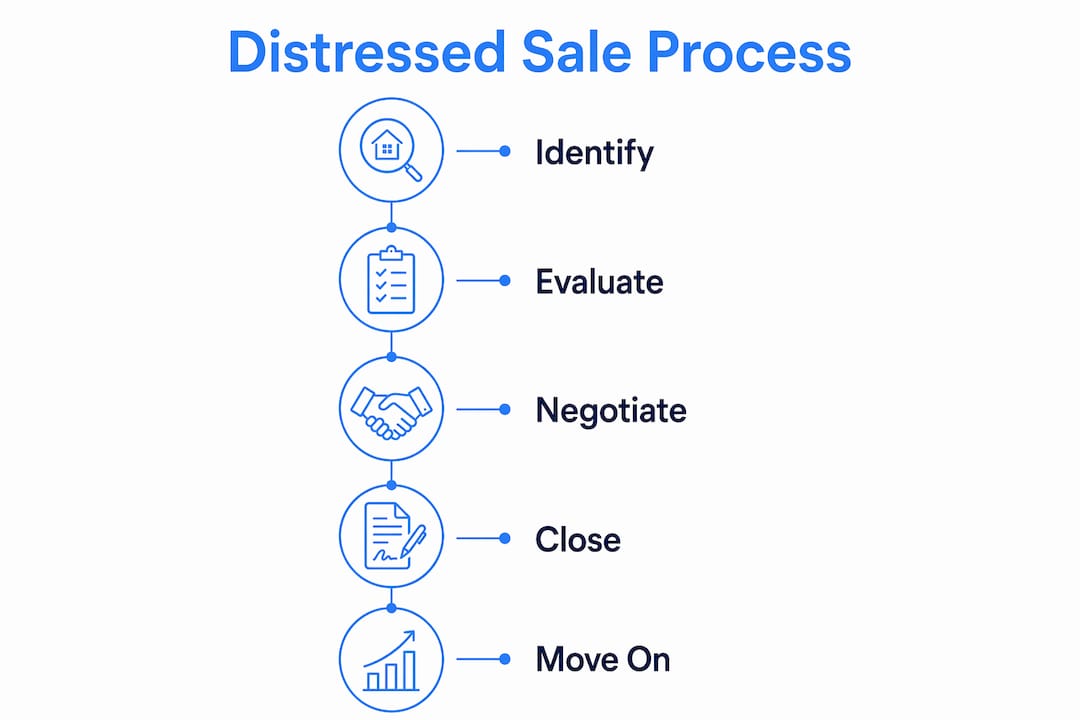

How does the distressed sale process work?

Not all distress sales follow the same path. The route you take determines your timeline, your negotiating position, and what rights you retain as a seller. Properly categorizing distressed sales by type helps you tailor your strategy and set realistic expectations.

Pre-foreclosure sales

Pre-foreclosure is the window between your first missed payment and the lender’s formal auction date. Pre-foreclosure sales close in 30–90 days and allow buyers to conduct inspections. Sellers retain more control here than at any later stage. You can negotiate directly with buyers, accept a cash offer, and avoid the public auction entirely. This route typically produces the best outcome for sellers who act early.

Short sales

A short sale happens when your mortgage balance exceeds what the home will sell for. The lender must approve the sale price because they are accepting less than what they are owed. Short sales require lender approval taking 30–120 days, and that timeline stretches further when multiple lienholders are involved. Short sales protect you from an outright foreclosure on your record, but they require patience and clear documentation.

Bank-owned (REO) and auction sales

Once a lender forecloses and takes ownership, the property becomes REO (real estate owned). Auctions and REO sales move fast, but they are sold strictly as-is with cash-only terms and no inspection rights. Sellers at this stage have lost most of their negotiating power. Buyers absorb the risk of unknown property conditions, which is why auction prices tend to be the deepest discounts in the distressed market.

| Sale type | Typical discount | Timeline | Financing allowed | Inspection rights |

|---|---|---|---|---|

| Pre-foreclosure | 5–15% below market | 30–90 days | Yes | Yes |

| Short sale | 10–20% below market | 30–120+ days | Sometimes | Usually |

| REO / bank-owned | 20–40% below market | 30–60 days | Cash preferred | Rarely |

| Auction | 20–40% below market | 7–30 days | Cash only | No |

Cash buyers can close a distressed sale in as few as 7 days. Lender-involved transactions can stretch to six months or longer. Knowing where you sit on that spectrum lets you plan accordingly.

What risks and legal issues do distressed sellers face?

Distress sales carry legal and financial consequences that outlast the closing date. Risks include deficiency judgments, surviving liens, credit damage, and title complications that affect both sellers and buyers. Ignoring these before you sign anything is a costly mistake.

Key risks every distressed seller should understand:

- Deficiency judgments: If your home sells for less than your mortgage balance, some states allow lenders to sue you for the difference. Anti-deficiency laws vary by state, so confirm your state’s rules before agreeing to any sale price.

- Surviving liens: IRS tax liens, mechanic’s liens, and secondary mortgages do not automatically disappear at closing. A buyer’s title company will surface these, and unresolved liens can kill a deal at the last minute.

- Credit impact: A short sale or foreclosure stays on your credit report for seven years. The damage affects your ability to rent, borrow, or qualify for a new mortgage.

- Title complications: Distressed properties often have clouded titles from unpaid taxes or unresolved estate claims. A thorough title and lien search before closing protects both parties from hidden liabilities.

- As-is buyer risks: Buyers purchasing distressed properties without inspections inherit unknown repair costs. Sellers benefit from this speed but should disclose known defects to avoid post-sale legal exposure.

Pro Tip: Consult a real estate attorney before accepting any offer on a distressed property. A one-hour consultation can prevent a deficiency judgment that follows you for years.

How should you approach selling a distressed property?

The best outcome in a distress sale comes from acting early and staying organized. Sellers in distress often prioritize quick resolution over maximizing price, which is understandable. But speed and value are not always mutually exclusive if you approach the process deliberately.

- Assess your timeline first. Count the days until your next legal deadline, whether that is a foreclosure auction date, a court order, or a tax sale. Your timeline determines which sale route is even available to you.

- Get a property condition assessment. Know what you are selling before a buyer tells you. A pre-sale inspection gives you leverage and prevents surprises that derail negotiations.

- Contact cash buyers and experienced investors early. Cash buyers facilitate fast sales of distressed homes with fewer contingencies. They close faster than financed buyers and are accustomed to as-is conditions.

- Communicate openly with your lender. If you are behind on payments, call your lender before they call you. Many lenders have loss mitigation departments that can pause foreclosure proceedings while a sale is arranged.

- Gather your documentation. Mortgage statements, tax records, title documents, and any existing liens should be organized before you accept an offer. Missing paperwork delays closings and costs you money.

- Negotiate on terms, not just price. A slightly lower price with a 10-day close can be worth more than a higher offer with 60-day financing contingencies when you are racing a legal deadline.

Pro Tip: If your property has code violations or disrepair issues, disclose them upfront. Buyers who specialize in distressed properties expect these conditions and will not walk away. Hiding them creates legal liability.

Understanding seller motivation is as important as understanding the property itself. The sellers who get the best outcomes are the ones who know exactly what they need and communicate that clearly.

Key Takeaways

A distressed seller is a homeowner forced to sell quickly due to urgent hardship, typically accepting 20–40% below market value to resolve a financial or personal crisis.

| Point | Details |

|---|---|

| Distressed seller definition | A homeowner pressured by hardship to sell fast, often at a significant discount from market value. |

| Common distress triggers | Foreclosure, divorce, bankruptcy, medical debt, and code violations each create different urgency levels. |

| Sale type determines timeline | Pre-foreclosure closes in 30–90 days; auctions can close in 7 days; short sales can take 6 months. |

| Legal risks are real | Deficiency judgments, surviving liens, and credit damage can follow sellers long after closing. |

| Act early for better outcomes | Sellers who engage cash buyers and lenders before deadlines hit retain more control and value. |

What I’ve learned from years of distressed seller conversations

Most people think distress selling is about the property. It is not. It is about the person. Every distressed seller I have encountered is managing a crisis that has nothing to do with square footage or comparable sales. They are managing fear, time pressure, and often a situation they did not choose.

The biggest mistake investors and wholesalers make is leading with price. Price is the last thing a truly distressed seller wants to talk about. What they want is someone who understands their situation and can show them a clear path out. Empathy and solving bottlenecks beyond price negotiation consistently produces better outcomes than any lowball offer strategy.

The sellers who respond best are the ones who feel heard before they feel sold to. That means asking about their timeline, their concerns, and what a good outcome looks like for them. The price conversation follows naturally once trust is established. Most profitable distressed deals come from early outreach before a property hits the public market, which means the conversation is everything.

If you are a seller reading this, know that the right buyer is not the one who offers the most. The right buyer is the one who can actually close on your timeline and solve your specific problem. If you are an investor or wholesaler, your job is to be that person. That skill is built through practice, not luck.

— Dave

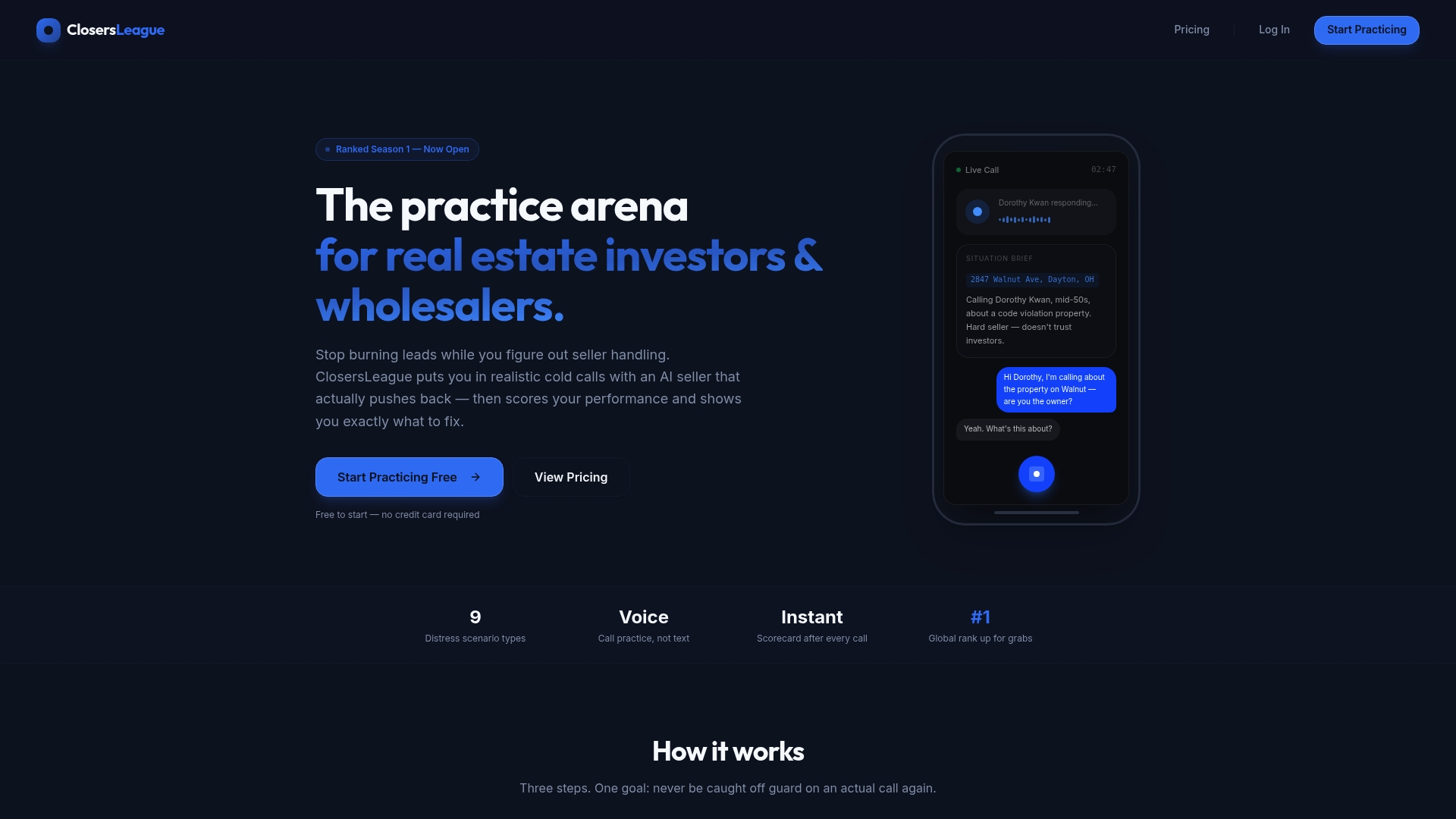

ClosersLeague trains you to have the right conversation

Knowing what a distressed seller is matters. Knowing what to say to one is what closes deals.

ClosersLeague is an AI-powered cold calling training platform built specifically for real estate investors and wholesalers. You practice real conversations with distressed sellers, including foreclosure, divorce, probate, and code violation scenarios, and get scored on empathy, objection handling, and communication clarity. The platform’s AI cold calling practice covers every major distressed seller type so you build confidence before you pick up the phone. If you work with inherited properties specifically, the inherited property roleplay module gives you targeted reps on one of the most emotionally complex seller situations in real estate. Stop winging it. Start drilling.

FAQ

What is a distressed seller in real estate?

A distressed seller is a homeowner who must sell quickly due to urgent financial or personal hardship, such as foreclosure, divorce, or bankruptcy. These sellers typically accept 20–40% below market value to resolve their situation fast.

What are the signs of a distressed seller?

Signs include missed mortgage payments, tax delinquency, code violations, probate filings, and properties listed well below neighborhood comps. Sellers who emphasize speed over price in conversations are also a strong signal.

How long does a distressed property sale take?

Timeline depends on the sale type. Cash buyers can close in as few as 7 days, pre-foreclosure sales typically close in 30–90 days, and short sales requiring lender approval can take 30–120 days or longer.

Can a distressed seller still negotiate?

Yes, especially in pre-foreclosure. Sellers retain negotiating power on price, closing date, and contingencies when they act before the lender takes control. The earlier you engage a buyer, the more leverage you keep.

What is the difference between a short sale and a foreclosure?

A short sale is seller-initiated with lender approval, allowing the seller to avoid foreclosure on their record. A foreclosure is lender-initiated after the seller defaults, resulting in the lender taking ownership and selling the property, usually at auction.