Distressed properties are real estate assets sold under seller duress, classified into four primary categories: financial, legal, physical, and situational distress. Each category contains specific property types with distinct seller motivations, timelines, and deal structures. Understanding the types of distressed properties gives you a real edge. Whether you are wholesaling, flipping, or buying to hold, knowing which category you are working with shapes every part of your approach, from your opening call to your offer price. Platforms like BatchData, PropertyReach, and DealRun have made identifying these properties faster than ever before.

1. What are the main types of distressed properties?

Distressed property is the industry’s informal term for what appraisers and lenders formally call “properties with impaired marketability.” The four categories are financial distress, legal distress, physical distress, and situational distress. Each one creates a different seller psychology and requires a different investor approach. Knowing which type you are dealing with before you pick up the phone is the difference between a productive conversation and a dead end.

2. Financial distress: pre-foreclosure, foreclosure auctions, and REO

Financial distress is the most recognized category and the one most investors target first. It includes pre-foreclosure, foreclosure auction, and bank-owned (REO) properties.

Pre-foreclosure is the window between a lender filing a notice of default and the property going to auction. Pre-foreclosure owners typically have 90–180 days before the auction date. That window creates real urgency, and sellers in this stage are often willing to accept below-market offers to avoid a public foreclosure on their record.

Foreclosure auctions happen when the owner cannot resolve the default. Properties sell to the highest bidder, often with no inspection period and no title guarantee. If a property goes unsold at auction, it reverts to the lender and becomes an REO.

REO (Real Estate Owned) properties are bank-owned assets. Banks are not in the business of managing real estate, so they price REOs to move. You deal directly with an asset manager, not an emotional homeowner. The process is slower but more predictable than an auction.

| Type | Seller | Timeline | Key Risk |

|---|---|---|---|

| Pre-foreclosure | Homeowner | 90–180 days | Owner may cure default |

| Foreclosure auction | Court/trustee | Single day | No inspection, title risk |

| REO | Bank/lender | 30–90 days | Slower negotiation |

Pro Tip: Aggregate data platforms with stackable filters outperform manual county record searches. Cost per record runs $0.05–$0.30, and you can layer default notices, tax delinquency, and skip-trace data in one pull. Use them to build your foreclosure lead pipeline before your competition does.

3. Legal distress: probate, divorce, bankruptcy, and liens

Legal distress properties are created by court processes or legal obligations that force a sale. These sellers are not always in financial trouble. They are often just stuck in a legal situation that makes holding the property painful.

The most common legal distress types include:

- Probate properties: Heirs inherit a home they did not plan for. Out-of-state heirs and divorce settlements push owners to liquidate quickly, often below market value. The property may sit vacant for months while the estate settles.

- Divorce sales: Courts often order the sale of jointly owned property during divorce proceedings. Both parties want it resolved fast, which creates real negotiating room for investors.

- Bankruptcy sales: A bankruptcy trustee’s job is to liquidate assets to pay creditors. Speed matters more than price in many of these cases.

- Tax liens and unpaid debt: A property with a tax lien attached is a signal that the owner is financially stretched. Lien-heavy properties can be purchased subject-to or negotiated with the lienholder directly.

Public records are your best tool for finding legal distress leads. Probate filings, lis pendens notices, and tax delinquency lists are all public documents available at the county courthouse or through data aggregators.

Pro Tip: When calling probate leads, lead with empathy. The seller just lost a family member. Your job is to uncover their real motivation before you ever mention price. Ask about their timeline and what a smooth sale would look like for them.

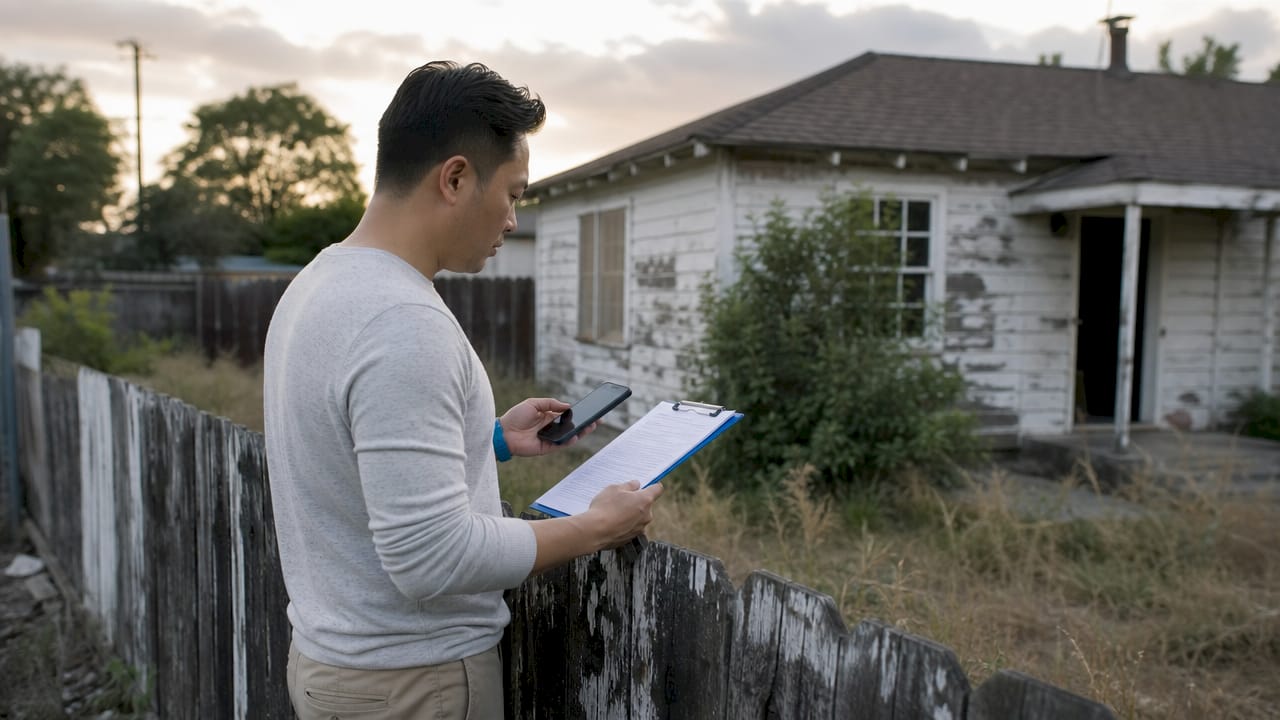

4. Physical distress: deferred maintenance, code violations, and rehab opportunities

Physical distress is about condition, not circumstance. These properties have visible problems that scare off retail buyers and make conventional financing impossible. That is exactly what makes them attractive to investors.

Common physical distress indicators include:

- Deferred maintenance: Roof failures, foundation cracks, HVAC systems past their useful life, and plumbing issues that have been ignored for years. Hazardous material removal or foundation issues can turn a profitable deal negative without thorough due diligence.

- Municipal code violations: A city-issued violation notice means the owner is on the clock. Fines accumulate daily in many municipalities. Owners who cannot afford repairs are highly motivated to sell.

- Renovation-needed properties: These are the classic rehab property category. They may not have active violations, but their condition disqualifies them from FHA or conventional loans.

Properties with code violations or foundation problems typically cannot qualify for conventional financing. That eliminates most retail buyers and leaves the field open for cash investors. The discount you negotiate must account for repair costs, carrying costs, and a realistic contingency buffer.

Pro Tip: Never estimate repair costs from the curb. Walk every room, pull permits, and get a contractor bid before you finalize your offer. Pricing repair risk accurately is the single most important skill in physical distress investing. A $10,000 underestimate on a foundation job can erase your entire margin.

ClosersLeague’s code violation cold calling practice lets you rehearse exactly how to open these conversations with owners who are frustrated, defensive, and under pressure from the city.

5. Situational distress: tired landlords, job relocation, and failed listings

Situational distress is the least obvious category and often the most profitable. The property itself may be in fine condition. The seller’s circumstances are what create the motivation to sell fast and at a discount.

Common situational distress types include:

- Tired landlords: A landlord who has managed a rental for 15 years, dealt with problem tenants, and deferred maintenance is often ready to exit at a price that works for you. They want simplicity, not top dollar.

- Job relocation: An owner who just accepted a job offer in another city needs to close fast. Carrying two mortgages is not an option. Speed is the value you bring.

- Failed MLS listings: A property that sat on the MLS for 90 or 120 days without selling is a signal. The seller has already experienced rejection. They are more open to a creative offer than they were on day one.

- Inherited properties with no attachment: Unlike probate, some heirs inherit properties they simply do not want. There is no grief, just a burden they want removed.

Off-market sourcing via direct mail or professional networks creates less competition and opens the door to creative deal structures like seller financing. Situational sellers often care more about terms than price. A full-price offer with a 90-day close loses to a slightly lower offer that closes in two weeks.

Knowing how to talk to tired landlords is a specific skill. The conversation is different from a foreclosure call. You are not solving a crisis. You are solving a fatigue problem.

6. Ways to find distressed properties across all categories

Finding distressed properties across all four categories requires a mix of data tools and direct outreach. No single method covers all types.

The most reliable ways to find distressed properties in 2026 include:

- Aggregate data platforms like BatchData and PropertyReach with layered filters for tax delinquency, default notices, and code violations

- County public records for probate filings, lis pendens, and tax lien lists

- Direct mail campaigns targeting specific distress signals by zip code

- Cold calling with scripts tailored to each seller type

- Driving for dollars to spot physical distress that has not yet appeared in any database

- MLS expired and withdrawn listings for situational distress leads

Signal stacking is the method experienced investors use to prioritize their outreach. A property with a tax lien, a code violation, and a missed mortgage payment is a far stronger lead than a property with just one of those signals. Combining multiple distress markers from public records dramatically increases the probability that a seller is motivated.

Pro Tip: Real estate prospecting tools that allow multi-market reach and skip tracing in a single platform cut your lead research time significantly. Build your list with stacked signals, then work it with consistent outreach.

7. Creative financing for distressed property deals

Creative financing is not optional in distressed investing. It is often the only way to close.

Bridge loans and creative financing enable faster closings on distressed properties. One documented case shows a bridge lender closing in three weeks versus the 60–90 days required by traditional lenders, resulting in a 120% value increase within 15 months. That speed advantage is the deal. Many distressed sellers will accept a lower price for a faster, more certain close.

Seller financing is another tool worth understanding. Off-market deals sourced through direct outreach often yield better terms than anything found on a public listing. When a tired landlord or a relocated owner does not need all their equity immediately, a seller-financed deal can work for both sides.

Know your financing options before you make your first call. Sellers ask about your ability to close. Your answer shapes their confidence in you.

Key takeaways

Distressed properties fall into four categories, and matching your outreach strategy to the specific type of distress is what separates profitable investors from those who spin their wheels.

| Point | Details |

|---|---|

| Four distress categories | Financial, legal, physical, and situational distress each require a different investor approach. |

| Pre-foreclosure window | Owners typically have 90–180 days before auction, creating a defined urgency window for investors. |

| Physical distress and financing | Code violations and foundation problems disqualify properties from conventional loans, attracting cash buyers. |

| Signal stacking improves leads | Layering multiple distress signals like tax liens and code violations identifies the most motivated sellers. |

| Speed closes situational deals | Situational sellers often value a fast, certain close over the highest possible price. |

What I have learned about distressed property investing

The category tells you everything before you dial

Most investors treat distressed properties as one big bucket. That is a mistake I see constantly. A probate seller and a pre-foreclosure seller are in completely different emotional states. One is grieving. The other is panicked. Walking into those calls with the same script is like using the same diagnosis for two different conditions.

The investors I have seen close the most deals are the ones who think like problem solvers first. Viewing yourself as a problem solver rather than just a buyer changes how you listen on a call. You stop waiting to pitch your price and start asking questions that reveal what the seller actually needs.

Signal stacking changed how I prioritize leads. A single tax lien is interesting. A tax lien plus a code violation plus a missed payment is a conversation I will make time for today. Combining multiple distress signals from public records is not just a data trick. It is a way to respect your own time.

My honest caution on physical distress deals: the repair cost estimate that kills you is the one you did not get a second opinion on. Foundation work and hazardous material removal have a way of expanding once the walls come down. Build a contingency into every physical distress offer. Not a small one.

Off-market sourcing through cold calling and direct mail still outperforms MLS hunting for distressed deals. The competition on a listed REO is real. The competition on a tired landlord you found through a tax delinquency list and called directly is almost zero.

— Dave

Practice the calls that close distressed deals

Knowing the categories is step one. Executing the conversation is where deals are won or lost.

ClosersLeague is an AI cold calling training platform built specifically for real estate investors and wholesalers. You can practice live roleplay scenarios for every distressed seller type covered in this article, including inherited property leads, code violation owners, tired landlords, and pre-foreclosure sellers. The AI scores your calls, flags objection-handling gaps, and lets you drill the same scenario until your response is automatic. Stop winging it on live calls. Use ClosersLeague’s cold calling practice platform to build the reps before the conversation counts.

FAQ

What is a distressed property?

A distressed property is a real estate asset sold under seller duress due to financial hardship, legal circumstances, poor physical condition, or situational factors. The seller is typically motivated to close quickly, often below market value.

What are the main types of foreclosure properties?

The main types of foreclosure properties are pre-foreclosure, foreclosure auction, and REO (bank-owned). Each stage offers different risks, timelines, and negotiation dynamics for investors.

How do investors find distressed properties off-market?

Investors find distressed properties through aggregate data platforms, county public records, direct mail, cold calling, and driving for dollars. Signal stacking, combining multiple distress indicators, identifies the highest-probability leads.

Why do physical distress properties attract cash buyers?

Properties with code violations or foundation problems cannot qualify for conventional financing. That eliminates most retail buyers and leaves the deal open for cash investors who can handle repairs.

What is situational distress in real estate?

Situational distress occurs when a seller’s personal or business circumstances, such as landlord fatigue, job relocation, or a failed listing, create motivation to sell quickly at a discount, regardless of the property’s physical condition.