A property comp, short for comparable sale, is a recently sold property with similar characteristics to your target property, used to estimate its current market value. Real estate professionals and appraisers rely on comps as the foundation of every serious valuation. Whether you’re a homebuyer negotiating a purchase price or an investor sizing up a distressed deal, understanding property comps is the difference between a confident offer and a costly mistake. Data sources like the MLS, Zillow, Redfin, and county public records all feed into this process.

What is property comps and why it matters

Property comps, formally called comparable sales or comparables, are the core tool in any property valuation method. The process works by identifying recently sold homes that a buyer could have reasonably purchased instead of your target property. That substitution test is the key. Not every recent sale qualifies; the main criterion is whether properties are genuine substitutes in the same immediate market area.

Comps serve multiple roles in a transaction. Buyers use them to avoid overpaying. Sellers use them to price competitively. Investors use them to calculate maximum allowable offers on acquisitions. Lenders and appraisers use them to confirm that a loan amount is supported by actual market evidence. Comps include active listings, in-contract properties, and recently sold homes to give you a full picture of where the market sits right now.

The formal term you’ll hear from appraisers is Comparative Market Analysis, or CMA. Real estate agents perform CMAs routinely, and licensed appraisers use a similar process called the Sales Comparison Approach under Uniform Standards of Professional Appraisal Practice. Both methods rely on the same underlying data: real, closed transactions between willing buyers and sellers.

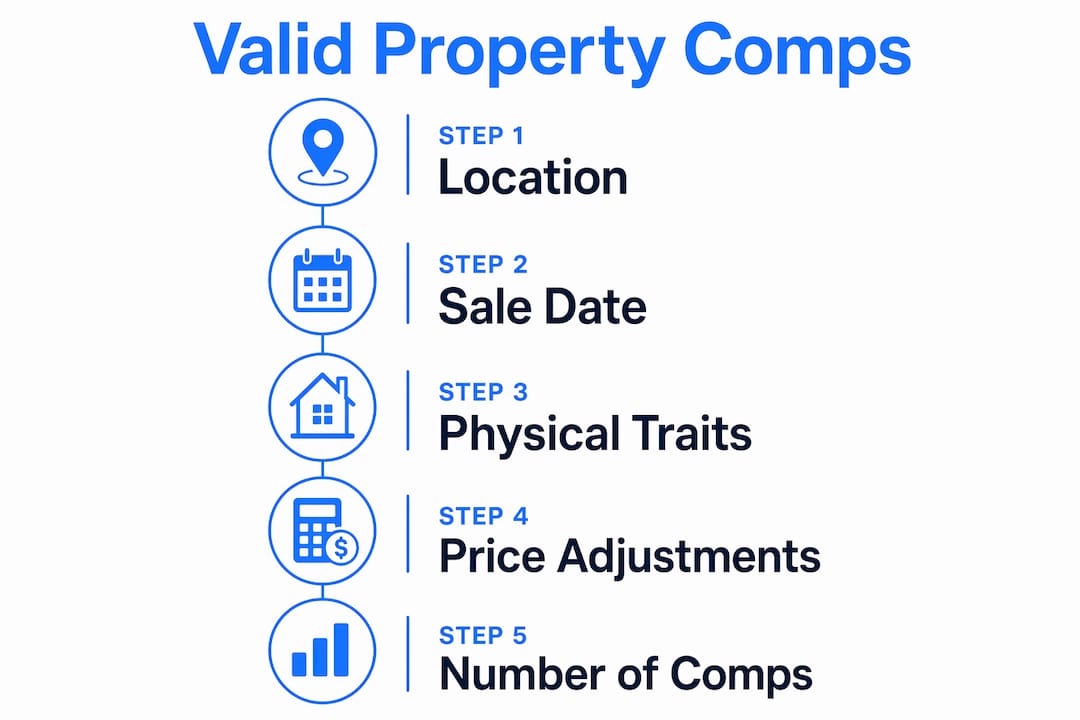

What criteria define a valid property comp?

Not every sold home in a zip code qualifies as a comp. The industry applies specific filters to make sure comparisons are meaningful.

Location and proximity are the first screen. The standard is a radius of 0.5 to 1 mile from the subject property in urban and suburban markets. In rural areas, that radius can expand to several miles, but the tighter the better. A comp two neighborhoods away may reflect a completely different school district, flood zone, or price tier.

Sale timeframe is equally critical. The accepted window is sales closed within the past 3 to 6 months. Markets move fast, and a sale from 18 months ago may reflect conditions that no longer exist. In rapidly appreciating or declining markets, some analysts tighten that window to 90 days.

Physical characteristics must align closely. The key attributes are:

- Property type (single-family, condo, townhouse, multi-family)

- Bedroom and bathroom count

- Gross living area in square feet (typically within 10 to 20 percent of the subject)

- Lot size for single-family homes

- Age and construction type

- Condition and any significant upgrades or renovations

Number of comps also matters for reliability. Using 3 to 6 comparable properties is the recommended range for a statistically sound analysis. Fewer than three reduces reliability significantly. More than six becomes difficult to manage manually and can introduce noise into the analysis.

Pro Tip: When you’re working distressed leads, such as probate or foreclosure properties, always note whether your comps are arm’s-length transactions. Bank-owned or auction sales often sell below market and can skew your valuation downward if used uncritically.

How to find property comps: tools and sources

Knowing where to pull comp data is as important as knowing what to look for. Here are the primary sources, ranked by reliability.

-

MLS access through a licensed agent. The Multiple Listing Service is the gold standard. Licensed agents use MLS data for the most accurate, up-to-date sales records, including days on market, final sale price versus list price, and seller concessions. If you work with an agent or have a broker relationship, this is your first call.

-

County assessor and recorder databases. Most counties publish deed transfers and sale prices in public records. Sites like your county assessor’s website or a state-level property search portal give you closed sale data without needing MLS access. The data is free but often lags by 30 to 90 days.

-

Zillow, Redfin, and Realtor.com. These platforms aggregate MLS and public record data and present it in a searchable format. Zillow’s Zestimate and Redfin’s Estimate are automated valuation models, not true comps. Use the sold listings filter directly rather than relying on their automated estimates. The raw sold data is useful; the algorithm-generated values are not a substitute for manual comp analysis.

-

PropStream, BatchLeads, and similar investor platforms. These tools are built specifically for real estate investors and pull from multiple data sources simultaneously. They let you filter by property type, sale date, square footage, and distance in one interface, which speeds up the comp-pulling process considerably.

-

Professional appraisers. For high-stakes acquisitions or when you need a defensible valuation for financing, a licensed appraiser produces a formal report using the Sales Comparison Approach. Agents use MLS and comparative market analysis to identify precise comps, but an appraiser’s report carries legal and lending weight that an agent’s CMA does not.

The DIY route using free tools works for quick screening. For serious investment decisions, especially on distressed properties where condition varies widely, professional-grade data sources pay for themselves.

How to analyze and adjust property comps for accurate valuation

Pulling comps is the easy part. Adjusting them correctly is where most investors and buyers make errors.

The core principle is this: adjustments are applied to the comp’s sale price, never to the subject property. You’re asking, “What would this comp have sold for if it were identical to my target property?” If a comp sold for $320,000 and has a pool that your subject property lacks, you subtract the pool’s market value from the comp’s price. If the comp is 200 square feet smaller than your subject, you add the per-square-foot value of that difference to the comp’s price.

Here is a simplified example of how adjustments work in practice:

| Feature | Subject property | Comp A | Adjustment to Comp A |

|---|---|---|---|

| Sale price | Unknown | $310,000 | Base |

| Square footage | 1,800 sq ft | 1,600 sq ft | +$20,000 |

| Bathrooms | 2 full | 2 full | $0 |

| Pool | No | Yes | -$15,000 |

| Adjusted comp value | $315,000 |

Once you’ve adjusted all your comps, you weight them. Comps that are most physically similar and require the fewest adjustments carry the most weight in your final value estimate. A comp that needed $50,000 in adjustments tells you far less than one that needed $5,000.

The output of a proper comp analysis is a value range, not a single number. Comps provide a credible price range to guide negotiation. If your adjusted comps cluster between $295,000 and $325,000, your subject property’s market value sits somewhere in that band. Pinning it to exactly $307,500 is false precision.

Pro Tip: Gather all potential comps within your criteria first, then filter down. Starting with fewer than three comps reduces reliability, while going beyond six makes manual analysis impractical. Cast wide, then tighten.

Common mistakes and pitfalls when using property comps

Even experienced investors fall into these traps. Knowing them in advance saves you from bad offers and worse deals.

- Comparing unlike properties. Using a condo as a comp for a single-family home, or a 1,200 square foot house as a comp for a 2,400 square foot house, produces meaningless results. The largest mistakes are comparing unlike properties and using outdated data.

- Relying on stale sales. A sale from 14 months ago in a market that has shifted 8 percent is not a valid comp. Always check the sale date and verify whether market conditions have changed materially since that transaction closed.

- Using too few comps. Three is the minimum for a defensible analysis. If you can only find one or two comps, expand your search radius slightly or extend your timeframe before making a major financial decision based on thin data.

- Treating list prices as market value. List prices are asking prices. Only closed sale prices reflect what buyers actually paid. Relying on active listings inflates your value estimate in a buyer’s market and understates it in a seller’s market.

- Ignoring seller concessions. If a seller paid $10,000 in closing costs for the buyer, the effective sale price was lower than the recorded number. MLS data often captures concessions; public records rarely do. This matters most when you’re trying to understand true net proceeds.

- Skipping condition adjustments. A fully renovated home and a property needing $40,000 in repairs are not the same comp, even if they share the same floor plan. Condition is a major value driver, especially on distressed acquisitions.

Key takeaways

Property comps are the most reliable tool for establishing market value, and using them correctly requires both the right data sources and disciplined adjustment methodology.

| Point | Details |

|---|---|

| Valid comp criteria | Comps must be sold within 3 to 6 months and located within 0.5 to 1 mile of the subject property. |

| Recommended comp count | Use 3 to 6 comps for a statistically sound and manageable valuation analysis. |

| Adjustment direction | Always adjust the comp’s sale price, never the subject property value, to reflect feature differences. |

| Weighting by similarity | Assign more weight to comps requiring the fewest adjustments to minimize valuation error. |

| Output is a range | Comps produce a credible value range for negotiation, not a single precise price point. |

Why comps are the investor’s real edge

I’ve reviewed hundreds of deals where the investor either overpaid or left money on the table, and in almost every case, the comp work was either skipped or done carelessly. People pull three Zillow sold listings, eyeball the prices, and call it a valuation. That’s not analysis. That’s guessing with extra steps.

The part most investors underestimate is the adjustment process. It feels tedious, but it’s where the real insight lives. When I’m working a probate lead or a tax-delinquent property, the condition gap between the subject and the comps can be $30,000 to $80,000. If you don’t account for that, your maximum allowable offer is wrong, and your deal math collapses at the closing table.

My honest advice: build a simple adjustment template and use it on every deal, even quick ones. It takes 20 minutes and forces you to think through the differences systematically. The discipline of doing it consistently is what separates investors who close profitable deals from those who chase volume and wonder why margins are thin. Comps also give you credibility on the phone. When you can tell a motivated seller exactly why you’re offering what you’re offering, grounded in real market data, the conversation changes. You’re not lowballing. You’re explaining. That shift in framing closes deals.

— Dave

Practice comp-informed conversations with ClosersLeague

Understanding comps is only half the equation. The other half is knowing how to use that data in a real conversation with a motivated seller.

ClosersLeague is an AI-powered cold calling training platform built specifically for real estate investors and wholesalers. You can practice inherited property cold calling scenarios where comp knowledge directly shapes your offer framing, or sharpen your skills on code violation leads where condition adjustments are the core of the negotiation. The platform scores your calls and gives you rep after rep until the comp-backed conversation feels natural. Stop winging your offers. Start drilling the dialogue that closes deals.

FAQ

What is a property comp in real estate?

A property comp is a recently sold home with similar characteristics to a target property, used to estimate its market value. Comps typically share similar square footage, bedroom count, location, and condition, and are sold within the past 3 to 6 months.

How many comps do you need for a reliable valuation?

Using 3 to 6 comparable properties is the recommended range for a sound valuation analysis. Fewer than three reduces reliability, while more than six becomes difficult to analyze manually.

Where can I find property comps for free?

Free sources include Zillow, Redfin, Realtor.com, and your county assessor’s public records database. For the most accurate data, a licensed real estate agent can pull comps directly from the MLS.

How do adjustments work when analyzing comps?

Adjustments are applied to the comp’s sale price, not the subject property. If a comp has a feature your property lacks, you subtract its value from the comp’s price. If your property has a feature the comp lacks, you add that value to the comp’s price.

What is the difference between a comp and a Zestimate?

A comp is a specific closed sale transaction used as direct market evidence. A Zestimate is an automated algorithm estimate generated by Zillow. Comps reflect actual buyer-seller negotiations; Zestimates are statistical models that can miss condition, upgrades, and local nuance significantly.