Foreclosure is defined as the legal process by which a mortgage lender seizes and sells a property after the borrower stops making payments and defaults on the loan. For homeowners facing missed payments, understanding what is foreclosure and how it unfolds can mean the difference between losing your home and finding a workable solution. Federal rules, state laws, and your own timing all shape the outcome. This article breaks down the foreclosure definition, the step-by-step process, the two main legal types, the real consequences, and the options available to you right now.

How does the foreclosure process work in the u.s.?

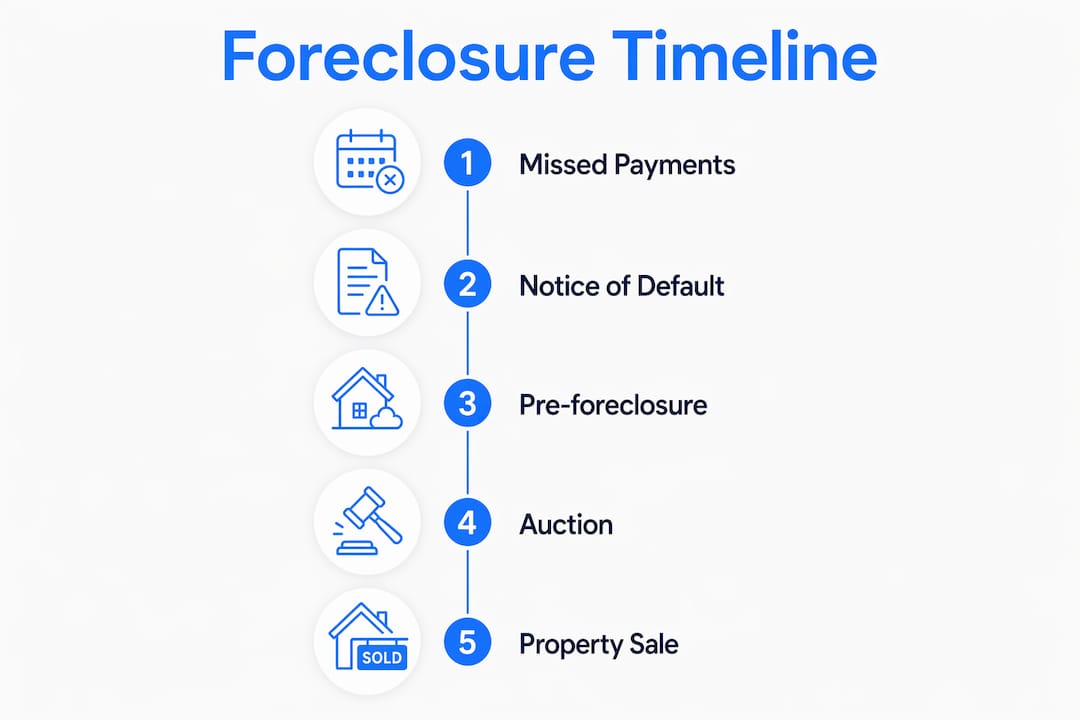

The foreclosure process follows a defined sequence of stages, not a single sudden event. Each stage gives you an opportunity to act. Knowing the order puts you in control.

Here is how the process typically unfolds:

- Missed payments begin. You fall behind on your mortgage. The clock starts ticking from your first missed payment.

- Servicer contact at day 36. Mortgage servicers must attempt live contact by day 36 of delinquency and provide written loss mitigation options by day 45. This is your first formal warning and your first real opening to negotiate.

- The 120-day federal floor. Servicers cannot initiate foreclosure until you are at least 120 days delinquent, per CFPB rules. That four-month window is your most valuable negotiating period.

- Notice of Default (NOD). After the 120-day mark, the lender files a formal notice of default. This is the official start of foreclosure proceedings.

- Waiting periods and notice of sale. State law governs notices and waiting periods between the NOD and the scheduled auction. These vary widely by state.

- Foreclosure sale or auction. The property is sold at public auction. If no buyer meets the minimum bid, the lender takes ownership and the home becomes REO (real estate owned) property.

Pro Tip: The 120-day window before formal foreclosure begins is your most powerful negotiating period. Contact your servicer before day 90 to maximize your options.

How long does foreclosure take by state?

Timeline is where foreclosure gets complicated. Non-judicial states average 2–8 months to complete foreclosure, while judicial states can take 6 to 24 months or more after the 120-day waiting period. A homeowner in Texas may face a completed foreclosure in under six months total. A homeowner in New York or New Jersey could remain in the process for two years or longer. Knowing your state’s typical timeline tells you how much time you actually have.

Judicial vs. non-judicial foreclosure: what is the difference?

The two main types of foreclosure in the U.S. are judicial and non-judicial. Which one applies to you depends on your state’s legal framework and, in some cases, the language in your mortgage documents.

Judicial foreclosure requires the lender to file a lawsuit in court to obtain a judge’s approval before selling the property. This process is slower and gives you more formal opportunities to contest the action. States like Florida, New York, and Illinois primarily use judicial foreclosure.

Non-judicial foreclosure allows the lender to proceed without court involvement, following a process defined in the deed of trust. It moves faster and gives homeowners fewer formal checkpoints to challenge the sale. States like California, Texas, and Arizona use this method. The Arizona foreclosure process is a clear example of how non-judicial procedures can move quickly once the notice of default is filed.

The legal theory underlying your state’s property law drives this distinction. Title theory states favor non-judicial foreclosure because the lender technically holds the title until the loan is paid off. Lien theory states, where the borrower holds the title and the lender holds only a lien, typically require judicial oversight.

| Feature | Judicial Foreclosure | Non-Judicial Foreclosure |

|---|---|---|

| Court involvement | Required | Not required |

| Typical timeline | 6–24+ months | 2–8 months |

| Homeowner’s right to contest | Stronger, formal legal process | Limited, faster process |

| Common states | Florida, New York, Illinois | California, Texas, Arizona |

| Redemption period | Often available | Varies, often shorter |

Pro Tip: Check your state’s foreclosure type before assuming how much time you have. A non-judicial state can move from notice of default to auction in as little as 90 days after the 120-day delinquency period ends.

What are the consequences of foreclosure for homeowners?

Foreclosure consequences extend well beyond losing the property. The financial and legal fallout can follow you for years. Here is what you need to know:

- Credit score damage. A foreclosure stays on your credit report for seven years. It typically drops your credit score by 100 to 150 points, making it harder to rent an apartment, finance a car, or qualify for a new mortgage.

- Deficiency judgment. If the foreclosure sale price is less than what you owe, the lender may sue you for the difference. Not every state allows this, but many do. You could owe tens of thousands of dollars even after the home is gone.

- Tax liability. The IRS may treat forgiven mortgage debt as taxable income. If your lender forgives a $50,000 deficiency, you could owe income tax on that amount unless an exemption applies.

- Future homeownership delays. FHA loans require a three-year waiting period after foreclosure. Conventional loans backed by Fannie Mae require seven years in most cases.

- Housing instability. After the sale, you must vacate the property. The timeline for eviction varies by state, but it adds stress and urgency to an already difficult situation.

The misconception that foreclosure ends with home loss overlooks the ongoing financial and credit consequences homeowners face afterward. The real cost of foreclosure is measured in years, not just the day of the sale.

Understanding these consequences is not meant to frighten you. It is meant to motivate early action, because every stage before the auction gives you a chance to reduce or eliminate these outcomes. For a broader look at what drives homeowners to this point, the ClosersLeague guide on distressed homeowner situations covers the full picture.

What options do homeowners have to avoid foreclosure?

Loss mitigation is the single most important defense against foreclosure. It refers to the set of options your servicer must evaluate before completing a foreclosure sale. Federal rules require servicers to review any complete loss mitigation application before moving forward.

Here are the most common options available to you:

- Forbearance. Your servicer temporarily reduces or pauses your payments. You still owe the missed amounts, but foreclosure is paused while you recover financially.

- Loan modification. Your servicer permanently changes the terms of your loan, such as lowering the interest rate or extending the repayment period, to make payments affordable again.

- Repayment plan. You catch up on missed payments over time by adding a portion of the overdue balance to your regular monthly payment.

- Short sale. You sell the home for less than you owe, with the lender’s approval. This avoids foreclosure on your record and often eliminates the deficiency balance.

- Deed in lieu of foreclosure. You voluntarily transfer the title to the lender in exchange for being released from the mortgage debt. It is faster and less damaging than a completed foreclosure.

Timing is critical. Submitting a complete loss mitigation application can legally pause foreclosure proceedings for 30 to 60 days during review. An incomplete application does not provide this protection. Get every document in order before you submit.

Many borrowers successfully avoid foreclosure by engaging with servicers early and applying for these programs before the 120-day mark. Waiting until after the notice of default is filed narrows your options significantly.

Pro Tip: Call a HUD-approved housing counselor before contacting your servicer. They are free, they know your servicer’s programs, and they can help you submit a complete application the first time. Find one at HUD.gov.

One more factor worth knowing: some servicers with high complaint rates engage in dual tracking, meaning they continue foreclosure proceedings while simultaneously reviewing your loss mitigation application. Research your servicer’s reputation and document every communication in writing. If you are also considering selling before the auction, the ClosersLeague resource on selling fast before foreclosure explains the timing and realistic options in detail.

Key takeaways

Foreclosure is a legal process with defined stages, federal protections, and real options for homeowners who act before the auction date.

| Point | Details |

|---|---|

| Federal 120-day rule | Servicers cannot start foreclosure until you are 120 days delinquent, giving you time to act. |

| Two foreclosure types | Judicial foreclosure takes longer and offers more legal recourse; non-judicial moves faster with fewer checkpoints. |

| Consequences extend beyond the home | Credit damage, deficiency judgments, and tax liability can follow you for years after the sale. |

| Loss mitigation pauses foreclosure | A complete application can legally halt proceedings for 30–60 days while your servicer reviews your options. |

| Early action is the best defense | Contacting your servicer before day 90 of delinquency maximizes the options available to you. |

The window most homeowners miss

Here is what I have seen repeatedly in working with distressed homeowners and the investors who call them: most people wait too long. They assume foreclosure is already decided the moment they miss a payment. It is not. The process has a built-in delay for a reason, and that delay is your leverage.

The 120-day federal window is not just a legal formality. It is a genuine negotiating period. Servicers have programs they are required to offer. Housing counselors can help you navigate them for free. The homeowners who come out of this process intact are almost always the ones who picked up the phone before the notice of default arrived, not after.

The other thing I would tell you directly: know your state. A homeowner in a judicial foreclosure state has fundamentally more time and more formal rights than someone in a non-judicial state. That difference shapes your entire strategy. If you are in California or Texas, you need to move faster. If you are in New York or Florida, you have more runway but also more complexity.

Do not treat foreclosure as a single event you either survive or do not. Treat it as a sequence of stages, each with its own decision point. That mindset shift alone changes what is possible.

— Dave

Practice the conversations that matter most

If you are a real estate investor or wholesaler working with homeowners in foreclosure, the quality of your first conversation determines everything. Homeowners in distress need to feel heard before they will consider any offer. That skill takes practice.

ClosersLeague is an AI-powered cold calling training platform built specifically for real estate investors and wholesalers. You can practice foreclosure cold calling scenarios with AI roleplay, get scored on your objection handling, and build the confidence to have real conversations with distressed sellers. Stop winging it. Start drilling the calls that close deals.

FAQ

What is the foreclosure definition in simple terms?

Foreclosure is the legal process a lender uses to take ownership of a property after the borrower stops making mortgage payments and defaults on the loan. The lender then sells the property to recover the unpaid debt.

How long does the foreclosure process take?

The foreclosure timeline depends on your state. Non-judicial states typically complete the process in 2–8 months, while judicial states can take 6 to 24 months or more after the mandatory 120-day delinquency period.

Can i stop foreclosure after it has started?

Yes. Submitting a complete loss mitigation application can legally pause foreclosure proceedings for 30 to 60 days. Options like loan modification, forbearance, or a short sale can stop or resolve the process entirely if pursued early.

What is the difference between judicial and non-judicial foreclosure?

Judicial foreclosure requires court approval and is slower, giving homeowners more formal rights to contest. Non-judicial foreclosure follows a lender-driven process defined in the deed of trust and moves significantly faster.

Does foreclosure affect your credit score?

A foreclosure stays on your credit report for seven years and typically reduces your credit score by 100 to 150 points. It also delays your ability to qualify for a new mortgage, with waiting periods ranging from three to seven years depending on the loan type.