Homeowners sell fast primarily because urgent personal circumstances force their hand, not because the market happens to be hot. The industry term for this is “motivated seller,” and understanding what drives motivation is the single most useful insight for anyone involved in a fast property transaction. Whether you are facing foreclosure, a sudden job transfer, or a divorce settlement deadline, the reasons for quick home sales almost always trace back to a specific life event colliding with a financial reality. This article breaks down those triggers, explains how pricing and financing shape the timeline, and gives you a practical framework for selling fast without leaving money on the table.

Why homeowners sell fast: the personal triggers that start everything

Urgent life and financial triggers such as foreclosure risk, job relocation, divorce, inheritance, and financial hardship are the most common reasons why homeowners sell fast. These are not abstract market forces. They are real deadlines with real consequences.

Here is what those triggers look like in practice:

- Foreclosure threat. A homeowner who has missed three mortgage payments faces a lender-initiated foreclosure timeline. Selling before the foreclosure completes protects their credit score and recovers whatever equity remains. The urgency of pre-foreclosure situations is one of the most time-sensitive scenarios in residential real estate.

- Job relocation. Corporate transfers often come with 30 to 60-day notice windows. A seller who needs to start a new role in another city cannot afford to wait six months for the right offer.

- Divorce and estate settlement. Courts set deadlines. When a judge orders a marital home sold as part of a divorce decree, or when an estate must be liquidated to distribute assets among heirs, the timeline is legally binding.

- Financial hardship. Medical bills, job loss, or mounting debt can make holding costs, including mortgage payments, property taxes, and insurance, unsustainable. Selling quickly stops the financial bleeding.

- Family changes and maintenance burden. An aging homeowner who can no longer maintain a property, or a family that has outgrown a home and needs to move before a school year starts, faces a practical deadline that is just as real as a legal one.

Life urgency compels homeowners to prioritize speed over price to avoid worsening outcomes such as credit damage and compounding stress. That trade-off is not irrational. It is a calculated decision to cut losses before they grow.

Pro Tip: If you are a real estate investor or wholesaler calling motivated sellers, uncovering seller motivation early in the conversation tells you exactly which trigger is driving urgency. That knowledge shapes every offer you make.

How do pricing, condition, and marketing affect sale speed?

Homes priced right, clean, maintained, and well-marketed meet buyer expectations from day one and attract quicker offers. This is the market-side equation that works alongside personal urgency.

Zillow’s data shows that 18.5% of U.S. homes went pending within seven days in February 2026, and those fast-selling homes were 2.6 times more likely to sell above asking price. Speed and price are not opposites when the home is positioned correctly. The median pending time for sold homes was 19 days, while typical active listings sat at 56 days, a 37-day gap that represents the cost of poor positioning.

Redfin warns sellers not to misinterpret market slowness as a reason to wait. Pricing relative to comparable homes, known as “comps,” remains the strongest single factor influencing how quickly a house sells.

| Factor | Impact on sale speed | What sellers can do |

|---|---|---|

| Pricing vs. comps | Highest impact; overpriced homes sit 37+ days longer | Price at or slightly below market from day one |

| Home condition | Clean, maintained homes attract faster offers | Address cosmetic repairs before listing |

| Staging and curb appeal | First impressions filter buyer interest within seconds | Invest in professional photos and basic staging |

| Marketing reach | Wider exposure shortens time to first offer | Use MLS, Zillow, and social media simultaneously |

| Location and supply | Low-inventory markets accelerate all timelines | Understand local absorption rate before pricing |

Pro Tip: Zillow’s economist notes that the best listings sell quickly because they align price and condition to buyer expectations from day one, even as broader market conditions cool. Do not wait for the market to come to you.

What role does financing type play in fast home sale timelines?

Fast sales involve two separate timing clocks. The first is the time from listing to accepted offer, which is driven by pricing and condition. The second is the time from accepted offer to closing, which is driven almost entirely by financing. Sellers should clarify which clock is urgent before choosing a sale strategy, because optimizing for the wrong clock wastes time.

Here is how the two financing paths compare:

- Cash buyers skip mortgage approval, appraisal contingencies, and underwriting. Cash sales close in as few as 7 to 14 days after offer acceptance. For a seller facing a foreclosure auction date or a court-ordered deadline, this difference is not a preference. It is the only viable path.

- Financed buyers require appraisal, inspection, and underwriting, each of which adds time and introduces a potential failure point. Financed purchases typically take 30 to 60 days or more to close. A loan denial at the underwriting stage can kill a deal entirely, forcing the seller to restart.

- As-is sales often attract cash buyers specifically because the seller is not making repairs. The trade-off in as-is home sales is a lower offer price in exchange for speed and certainty.

| Financing type | Typical close time | Key delay risks | Best for |

|---|---|---|---|

| Cash offer | 7 to 14 days | Title issues, seller documentation | Foreclosure, divorce, estate deadlines |

| Conventional loan | 30 to 45 days | Appraisal gaps, underwriting | Standard market sales |

| FHA or VA loan | 45 to 60 days | Stricter appraisal standards | Buyers with lower down payments |

Opendoor’s data confirms that cash sales reduce lender contingency risks that can derail financed deals, which is critical when sellers face real deadlines. The speed advantage of cash is not just about calendar days. It is about deal certainty.

How can homeowners sell fast without sacrificing value?

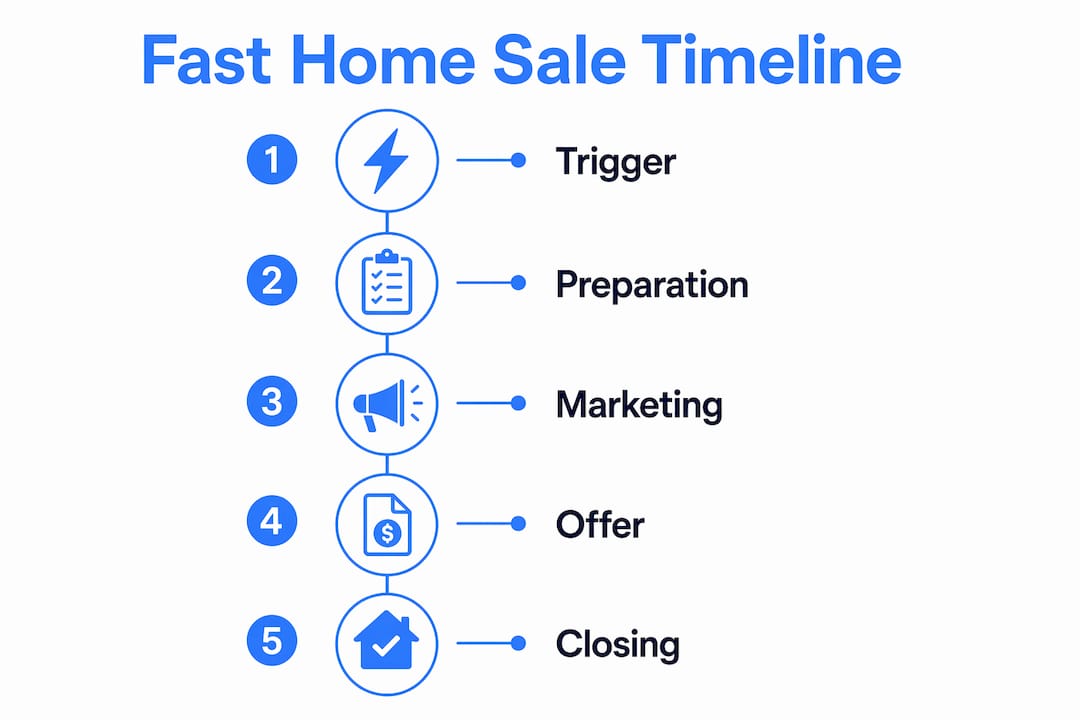

Selling fast and selling smart are not mutually exclusive. The sellers who lose the most money are those who react emotionally to urgency instead of managing it strategically. Here is a numbered framework that keeps both speed and value in focus:

-

Set a concrete deadline date. Vague goals like “sell soon” lead to indecision and wasted time. Setting a clear deadline date forces you to choose the right method from the start. Cash sales close in roughly 7 to 21 days after acceptance. Financed sales take 30 to 45 days. Work backward from your deadline to decide which path is realistic.

-

Price from the data, not from emotion. Pull comps for homes sold within the last 90 days in your zip code. Price at or slightly below that range. Overpricing by even 5% can add weeks to your timeline and signal desperation when you eventually reduce.

-

Prepare the home to meet buyer expectations efficiently. You do not need a full renovation. Clean, declutter, fix visible defects, and invest in professional listing photos. Buyers form opinions in seconds, and a strong first impression shortens the time to offer.

-

Manage contingency risks proactively. Late-stage contingencies like appraisal or underwriting gaps can stall even deals that look fast on paper. If you accept a financed offer, ask for a pre-approval letter from a reputable lender and request a short inspection period upfront.

-

Match your sale method to your urgency level. If your deadline is under 21 days, pursue cash buyers and consider as-is sale options explicitly. If you have 45 days or more, a traditional listing with strong marketing will likely produce a higher net price.

Pro Tip: Real estate investors and wholesalers who practice distressed seller call scenarios understand this framework from the buyer side. Knowing how sellers think about these five steps makes you a far more effective negotiator.

Key takeaways

Homeowners sell fast because urgent personal circumstances create real deadlines, and the fastest sales happen when pricing, condition, and financing type all align with that urgency from day one.

| Point | Details |

|---|---|

| Personal urgency drives speed | Foreclosure, divorce, relocation, and financial hardship are the top triggers for motivated sellers. |

| Pricing is the strongest market lever | Homes priced at or below comps go pending 37 days faster than overpriced listings. |

| Cash closes in 7 to 14 days | Cash buyers eliminate appraisal and underwriting delays, making them the fastest path to closing. |

| Two clocks govern every sale | Time to offer and time to close require separate strategies; sellers must know which is urgent. |

| Speed and value can coexist | Strategic pricing, preparation, and contingency management protect sale price even under tight timelines. |

What I’ve learned from watching sellers make the same mistakes

I have spent years listening to homeowners describe their situations on cold calls, and the pattern is consistent. Sellers who wait too long to acknowledge their urgency almost always end up with worse outcomes than those who act decisively early. A homeowner who admits they need to sell in 30 days and prices accordingly will net more than one who lists at an aspirational price for 90 days and then panics into a cash offer at a steep discount.

The other misconception I see constantly is that accepting a cash offer means getting robbed. That is not accurate. Cash offers are lower than financed offers in most cases, but the certainty and speed have real financial value. Holding costs on a vacant property, including mortgage, taxes, insurance, and utilities, can run $2,000 to $4,000 per month depending on the market. A cash offer that closes in 10 days versus a financed offer that closes in 45 days represents 35 days of holding costs saved, plus the risk premium of a deal that might fall through at underwriting.

The sellers I respect most are the ones who separate emotion from math. They know their deadline, they know their number, and they choose the method that gets them to both. That clarity is not something most people arrive at naturally. It usually takes a direct conversation with someone who asks the right questions.

— Dave

How ClosersLeague helps investors connect with motivated sellers

Understanding why homeowners sell fast is only half the equation. The other half is knowing how to have the right conversation when you reach one. ClosersLeague is an AI-powered cold calling training platform built specifically for real estate investors and wholesalers who work with motivated sellers in foreclosure, probate, divorce, and other distressed situations. The platform uses AI roleplay to simulate real seller objections and emotional states, so you practice handling urgency, hesitation, and price resistance before it costs you a deal. Stop winging it on live calls. Start drilling with AI cold calling practice built for every seller type you will actually encounter.

FAQ

What are the most common reasons homeowners sell fast?

Foreclosure risk, job relocation, divorce, estate settlement, and financial hardship are the top triggers. These create real deadlines that make speed a higher priority than maximizing sale price.

How quickly can a home actually close?

Cash sales close in as few as 7 to 14 days after offer acceptance. Financed sales typically take 30 to 45 days, with FHA and VA loans often running 45 to 60 days due to stricter appraisal requirements.

Does selling fast mean selling for less?

Not always. Homes priced correctly and well-presented can sell within a week and still close above asking price. The price discount typically applies to as-is or cash-only sales where the seller trades value for speed and certainty.

What is the biggest risk in a fast home sale?

Late-stage contingencies, particularly appraisal gaps and underwriting denials in financed deals, are the most common reasons fast sales stall. Accepting a cash offer eliminates most of these risks.

How should a homeowner choose between a cash offer and a traditional listing?

Set a concrete deadline date first. If you need to close within 21 days, pursue cash buyers. If you have 45 or more days, a traditional listing with strong marketing will likely produce a higher net price after holding costs are factored in.