A pre-foreclosure call approach is a systematic method for contacting homeowners who have received a Notice of Default, with the goal of opening a conversation before the property reaches auction. The industry term for this outreach is distressed seller prospecting, and the pre-foreclosure window is one of the most time-sensitive opportunities in real estate investing. The best results come from combining early contact, empathetic communication, and a structured follow-up cadence. Platforms like EquityTier and FlipMantis have documented that most deals close between the 3rd and 8th contact attempt. That means persistence, paired with the right message, is what separates investors who close deals from those who burn through lists.

What makes timing critical in the pre-foreclosure call approach?

The optimal outreach window is within 1–2 weeks after a Notice of Default is filed. At that stage, homeowners are stressed but not yet overwhelmed by competing solicitations. They are still weighing options and are more open to a calm, informative conversation.

As the auction date approaches, two things happen. The homeowner’s anxiety spikes, and their inbox fills with mailers and calls from other investors. Your ability to stand out drops sharply. Contacting a homeowner 90 days before auction is a fundamentally different conversation than calling them 10 days out.

Regional legal deadlines also shape your timing. Some states give homeowners a right of redemption period after a sale, while others move from filing to auction in as few as 90 days. Knowing your state’s foreclosure timeline is not optional. It directly determines how many contact attempts you can realistically make before the deal window closes.

- Contact within 1–2 weeks of the Notice of Default filing

- Avoid the final 2 weeks before auction, when homeowner stress peaks

- Map your state’s foreclosure timeline before building your outreach schedule

- Track filing dates in your CRM so no lead ages past its prime window

Pro Tip: Set a calendar alert for every new lead at the 7-day and 30-day marks after the filing date. This keeps you in the early window without relying on memory.

What are the most effective call scripts for pre-foreclosure homeowners?

Empathy-led, consultative approaches outperform sales-driven tactics when contacting distressed homeowners. The homeowner is not thinking about your deal. They are thinking about their family, their credit, and whether they can stay in their home. Your opening line needs to reflect that reality.

The single most important language rule: avoid the word “foreclosure” in your opening. Referencing the property situation rather than the filing directly reduces defensive reactions and improves your connect-to-conversation rate. Say “I noticed there was a filing related to your property on Oak Street” instead of “I see your home is in foreclosure.” The second phrase triggers a wall. The first opens a door.

Your call structure should follow this sequence:

- Opening: Reference the specific property and filing, not the foreclosure label

- Acknowledgment: Validate that the situation is stressful and that you are not there to pressure them

- Listening: Ask open questions and let the homeowner talk. Gather information on their timeline, equity, and intentions

- Options: Present multiple paths, including loan modification, listing, and a cash sale, so they feel in control

- Qualifying questions: “Are you currently working with your lender on any options?” and “What would need to happen for you to feel good about the next step?”

Explaining credit score impacts of foreclosure versus a short sale or cash sale builds your credibility fast. Most homeowners do not know the difference. Being the person who explains it positions you as a knowledgeable partner, not a vulture.

Pro Tip: Position your cash offer as a backup plan, not the primary pitch. Most homeowners are pursuing loan modifications and need to feel that option is respected before they will consider yours.

How to design a multi-touch follow-up cadence for pre-foreclosure leads

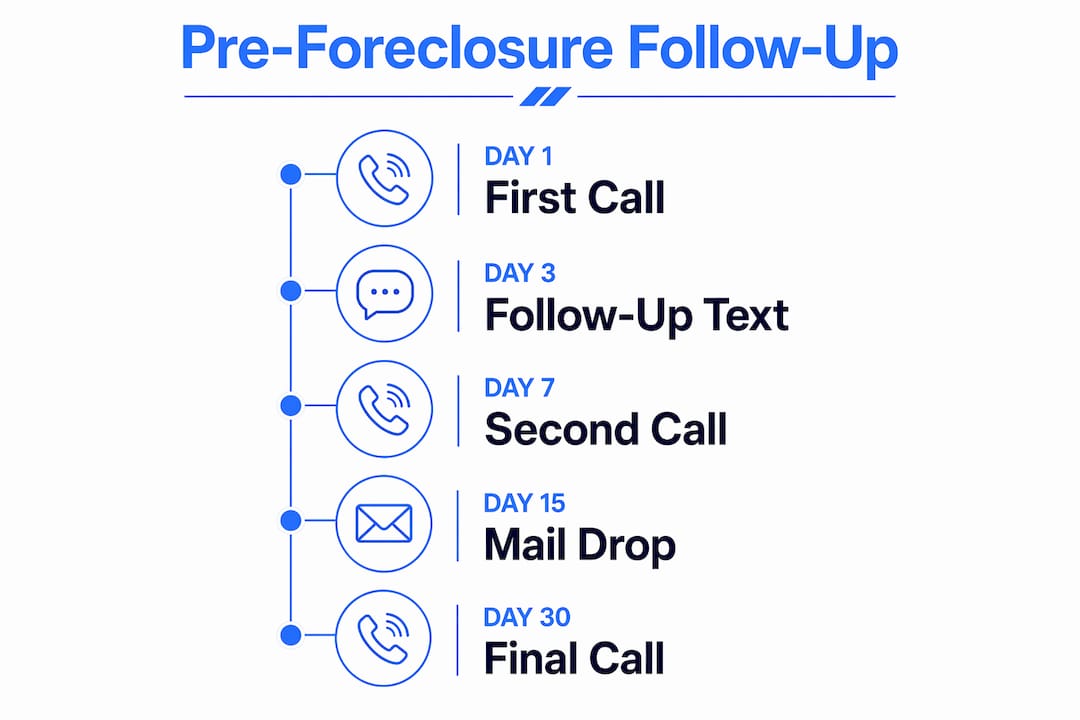

Most investors quit after one or two calls. That is the single biggest mistake in pre-foreclosure outreach. Data from EquityTier confirms that deals close between the 3rd and 8th contact, which means your follow-up system is as important as your opening script.

A proven cadence balances calls, texts, and physical mail to stay present without becoming a nuisance. Each contact type serves a different purpose in the relationship-building process.

| Day | Contact Type | Purpose |

|---|---|---|

| Day 1 | Call | First introduction, establish tone and empathy |

| Day 3 | Call | Follow up, answer questions, build rapport |

| Day 5 | Text | Low-pressure check-in, easy to respond to |

| Day 7 | Call | Deeper conversation, explore options |

| Day 14 | Call | Reassess homeowner situation and timeline |

| Day 21 | Direct mail | Physical touchpoint, reinforces credibility |

| Day 30+ | Monthly call or mail | Long-term nurture for undecided homeowners |

Texts work well mid-cadence because they require less commitment from the homeowner to respond. A simple “Hi, this is [your name]. Just checking in on the Oak Street property. Happy to chat when the time is right.” carries no pressure and keeps your name visible.

Opening lines referencing the specific property rather than asking generic questions produce measurably higher connect-to-conversation rates. Apply that same specificity to your texts and mail pieces.

Pro Tip: Adjust the cadence based on homeowner responsiveness. If someone replies to your Day 5 text, move your Day 7 call forward. If someone asks you not to call, shift to mail only. Respecting boundaries keeps the door open.

What legal and regulatory rules apply to pre-foreclosure outreach?

Legal compliance is not a detail you handle later. It is a foundational part of your outreach strategy. Getting it wrong can void contracts, trigger penalties, and destroy your reputation in a market.

State laws often require a 5-day rescission window for contracts signed after foreclosure-related outreach. This means a homeowner can cancel a signed agreement within five days in many states. Ignoring this rule does not make it go away. It makes your deal unenforceable.

Federal rules also apply. If a homeowner submits a complete loss mitigation application more than 37 days before auction, regulations require the foreclosure process to pause. That directly affects your negotiation timeline and the urgency you can reasonably communicate.

Key compliance points every investor must address:

- Consult a local real estate attorney before running outreach campaigns in a new state

- Know your state’s Equity Skimming and Foreclosure Rescue laws, which restrict certain investor practices

- Include required disclosures in written communications, especially direct mail

- Never misrepresent your role, your offer, or the homeowner’s options

- Avoid language that implies the homeowner has no other choice

The ethical dimension matters beyond legal compliance. Validating a seller’s efforts to keep their home before presenting a sale offer builds trust and makes eventual deal closure more likely. Predatory tactics produce short-term deals and long-term reputation damage.

How to use data and tools to prioritize your outreach

Not all pre-foreclosure leads are equal. A homeowner with 40% equity in their property is a fundamentally different conversation than one who is underwater on their mortgage. Your data should shape your script before you dial.

Start with equity position. High-equity leads are candidates for straightforward cash purchases. Zero-equity or negative-equity leads may be better suited for subject-to deals or short sale negotiations. Pulling this data before the call lets you tailor your opening and your offer type from the first sentence.

Lead sources like EquityTier and FlipMantis provide filing dates, owner contact information, and in some cases loan balance estimates. Pair that data with a CRM to track every contact attempt, note homeowner responses, and flag leads for follow-up at the right cadence stage. Without a CRM, your follow-up system falls apart at scale.

Key metrics to track across your outreach:

- Contact rate: how many dials result in a live conversation

- Conversation-to-appointment rate: how many conversations lead to a follow-up meeting

- Appointment-to-offer rate: how many meetings result in a submitted offer

- Days from first contact to signed contract: measures your cadence efficiency

Automated dialers reduce dead time between calls and increase your daily contact volume. Pair them with a script loaded in your CRM so you are never caught off guard. For a full breakdown of how to source and prioritize leads, the foreclosure leads guide from ClosersLeague covers timing and data-driven techniques in detail.

You should also track whether a homeowner has listed their property or applied for a loan modification. That information changes your pitch entirely. A homeowner who just listed with an agent needs a different conversation than one who has not taken any action yet.

Key Takeaways

The most effective pre-foreclosure call approach combines early outreach within 1–2 weeks of a Notice of Default, empathetic language that avoids triggering terms, and a structured multi-touch follow-up cadence that persists through the 3rd to 8th contact attempt.

| Point | Details |

|---|---|

| Time your first call early | Contact homeowners within 1–2 weeks of the Notice of Default filing for the best response rates. |

| Avoid triggering language | Reference the property situation, not the word “foreclosure,” to reduce defensive reactions. |

| Follow up 3–8 times | Most deals close between the 3rd and 8th contact, so a structured cadence is non-negotiable. |

| Know your state’s laws | Rescission periods and Foreclosure Rescue laws vary by state and can void contracts if ignored. |

| Use equity data to tailor offers | Match your offer type to the homeowner’s equity position before you dial. |

What I’ve learned after years of watching investors blow pre-foreclosure calls

Most investors treat pre-foreclosure calls like a numbers game. Dial enough people, and eventually someone says yes. That mindset produces mediocre results at best and burned bridges at worst.

The investors who consistently close pre-foreclosure deals share one trait: they genuinely care about solving the homeowner’s problem. That is not a soft skill. It is a competitive advantage. A homeowner in distress can detect a scripted pitch in the first 10 seconds. They have heard it before. What they have not heard is someone who asks a real question and then actually listens to the answer.

The biggest mistake I see is rushing to present an offer before understanding the homeowner’s situation. You cannot build a relevant offer without knowing their timeline, their equity, their relationship with their lender, and what they actually want to happen. Skipping that discovery phase is why so many calls end with “not interested” before the investor even gets to their pitch.

Refining your script based on real call feedback is the only way to improve. Record your calls where legally permitted. Listen back. Notice where homeowners go quiet, where they push back, and where they open up. That data is more valuable than any script template you can buy. ClosersLeague’s cold calling distressed homeowners guide covers the consultative approach in depth, and it is worth reading alongside your own call recordings.

Treat every pre-foreclosure homeowner as a person navigating one of the hardest moments of their financial life. That posture will make you a better caller, a better negotiator, and a more trusted investor in your market.

— Dave

ClosersLeague: practice your pre-foreclosure calls before they count

Knowing the right approach is one thing. Delivering it under pressure on a live call is another. ClosersLeague is an AI-powered cold calling training platform built specifically for real estate investors and wholesalers who want to get better at talking to distressed homeowners.

The platform simulates real pre-foreclosure conversations, including objections, emotional responses, and difficult questions, so you can practice your script, sharpen your empathy, and build confidence before you dial a real lead. You can run AI cold calling practice sessions tailored to foreclosure, probate, divorce, and other distressed seller scenarios. Stop winging it. Start drilling.

FAQ

When is the best time to call a pre-foreclosure homeowner?

The best window is within 1–2 weeks after a Notice of Default is filed. Contact rates and homeowner openness drop significantly as the auction date approaches.

What should I avoid saying on a pre-foreclosure call?

Avoid using the word “foreclosure” in your opening. Reference the property filing or situation instead, which reduces defensive reactions and keeps the conversation open.

How many times should I follow up with a pre-foreclosure lead?

Follow up at least 3–8 times across calls, texts, and mail. Most deals in pre-foreclosure outreach close between the 3rd and 8th contact attempt.

Are there legal rules I must follow when calling pre-foreclosure homeowners?

Yes. Many states require a 5-day rescission period for contracts signed after foreclosure-related outreach. Consult a local attorney before running campaigns in any new state.

How do I know what offer to make on a pre-foreclosure property?

Pull the homeowner’s equity position before you call. High-equity properties suit cash purchases, while zero-equity situations may call for subject-to deals or short sale negotiations.