A cash offer in real estate is defined as a purchase proposal where the buyer uses liquid funds to buy a property without any mortgage or lender involvement. This structure removes the bank from the transaction entirely, which changes the speed, risk, and negotiation dynamics for everyone at the table. Approximately 33% of all U.S. home sales in 2026 are all-cash transactions. That number tells you cash offers are not a niche tactic reserved for wealthy investors. They are a standard part of the American real estate market that every buyer and seller needs to understand.

What is a cash offer and how does it work?

A cash offer means the buyer has liquid funds ready to transfer at closing, with no mortgage application, no underwriting, and no lender approval required. The industry term for this is an “all-cash transaction,” and it is the recognized standard used by the National Association of Realtors (NAR) and real estate attorneys nationwide.

The process follows a clear sequence:

- Buyer identifies the property and submits a written purchase offer stating they will pay with cash.

- Buyer provides a proof of funds letter from their bank or financial institution. This document replaces the mortgage pre-approval letter used in financed deals.

- Seller reviews and accepts the offer, often skipping the appraisal contingency entirely.

- Escrow opens and both parties sign the purchase agreement. The buyer deposits earnest money.

- Buyer wires the full purchase amount to the escrow or title company before the closing date.

- Title transfers and the deal closes, typically within 7 to 14 days compared to the standard 30 to 60 days for financed purchases.

One critical clarification: cash does not mean physical bills. A cash offer requires liquid assets held in checking, savings, or money market accounts. Funds tied up in stocks, retirement accounts, or pending home sale proceeds generally do not qualify until they are liquidated and accessible.

Some buyers use bridge loans or HELOCs to fund cash offers without placing a lien on the new property. This preserves the key advantage of a cash offer while allowing buyers to access capital they have not yet freed up from other assets.

Pro Tip: If you plan to use a HELOC or bridge loan to make a cash offer, confirm with your lender that the funds will be available before you submit the offer. Sellers will ask for proof of funds immediately.

What are the benefits and drawbacks of cash offers?

Cash offers carry real advantages for both sides of the transaction, but they also come with trade-offs that are worth understanding before you commit.

Benefits for sellers

- Faster closing. Cash deals close in 7 to 14 days, which matters enormously for sellers facing foreclosure, probate deadlines, divorce settlements, or job relocations.

- Higher certainty. Cash offers remove lender approval contingencies, which means the deal is far less likely to fall through at the last minute.

- Fewer contingencies. Cash buyers typically waive appraisals and make fewer repair demands, which simplifies the entire transaction.

- Less stress. No waiting on an underwriter, no last-minute loan denials, and no appraisal surprises.

Drawbacks for sellers

- Lower price. Cash buyers frequently expect a 5% to 15% discount below market value. They price in the speed and convenience they are providing.

- Investor motivation. Cash buyers are often investors or flippers focused on return on investment, not sentimental value. Their offers reflect that math.

Benefits and drawbacks for buyers

Cash buyers gain a strong competitive edge in multiple-offer situations. Sellers consistently prefer the certainty of a cash deal over a higher financed offer with more risk. The drawback is real: you need full liquidity, which means that capital is no longer working for you in investments or other assets. For buyers who can afford it, the trade-off is often worth it in competitive markets.

Pro Tip: As a seller, weigh the price difference against your timeline and risk tolerance. A cash offer that closes in 10 days with no contingencies may be worth more to you than a financed offer that is $15,000 higher but carries a 45-day close and appraisal risk.

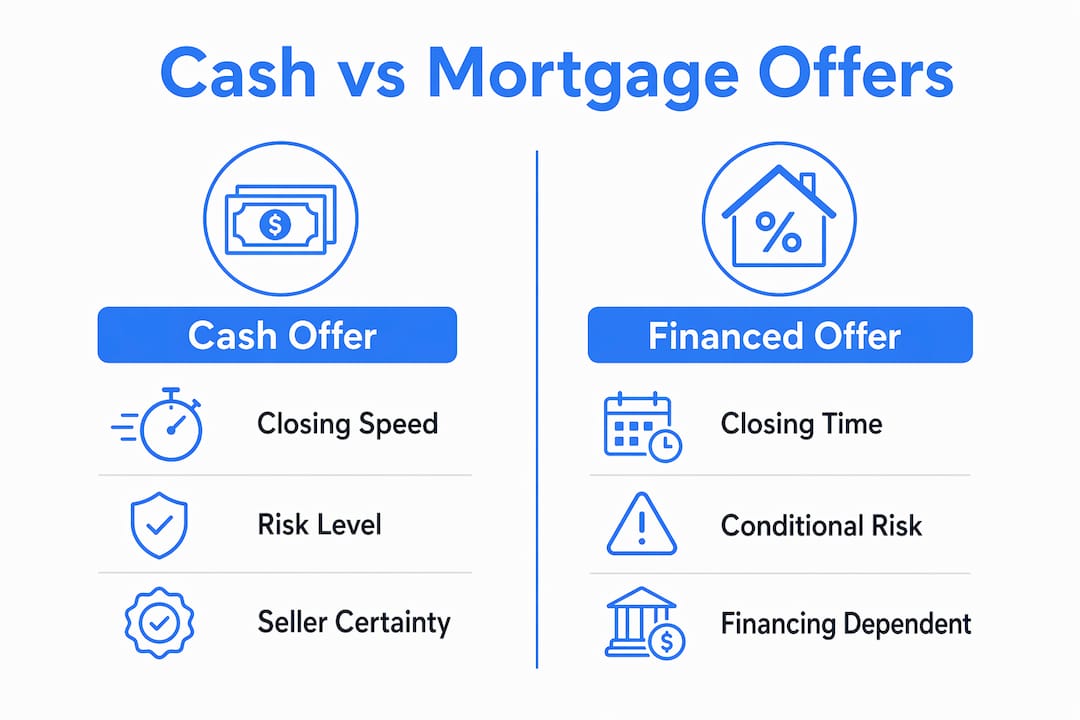

How does a cash offer compare to a financed mortgage offer?

The core difference between a cash offer and a mortgage offer comes down to risk and time. Understanding that difference helps sellers make smarter decisions when they receive multiple offers.

| Factor | Cash offer | Financed (mortgage) offer |

|---|---|---|

| Closing timeline | 7–14 days | 30–60 days |

| Lender contingency | None | Required |

| Appraisal requirement | Usually waived | Required by lender |

| Deal fall-through risk | Very low | Moderate to high |

| Typical price | 5%–15% below market | Closer to market value |

| Documentation required | Proof of funds letter | Mortgage pre-approval |

The risk profile is the most important column in that table. A financed offer can collapse at multiple points: the buyer’s loan application can be denied, the appraisal can come in below the purchase price, or underwriting can stall the deal for weeks. A cash offer eliminates all of those failure points.

If the gap between a cash offer and a financed offer is less than 5%, experts recommend choosing the cash offer. The certainty and speed outweigh the small price difference. When the gap is larger, sellers need to honestly assess how much risk and delay they can absorb.

For sellers dealing with distressed situations like foreclosure or probate, the speed advantage of a cash offer is often the deciding factor. You can learn more about why sellers choose speed and what drives those decisions in different life circumstances.

What practical steps should sellers and buyers take with cash offers?

Knowing the theory is one thing. Executing a cash transaction without costly mistakes is another. Here is what both sides need to do.

For sellers

- Verify proof of funds immediately. Ask for a bank statement or official letter dated within the last 30 days. Do not accept screenshots or informal documents.

- Negotiate contingencies upfront. Even cash buyers may include an inspection contingency. Decide which contingencies you will accept before you counter.

- Plan your move-out timeline. Cash deals can close in as few as 7 to 10 days, which leaves little time to relocate. Negotiate a leaseback or rent-back agreement if you need more time in the home after closing.

- Get everything in writing. Verbal agreements about closing dates or repairs mean nothing. Every term belongs in the purchase contract.

For buyers

- Consolidate your liquid funds before you make an offer. Move money from savings, money market accounts, or liquidated investments into one accessible account. Sellers and escrow companies need to see clean, verifiable funds.

- Draft your proof of funds letter with your bank. This letter should show the account balance, the account holder’s name, and the date. Most banks can produce this within 24 hours.

- Understand the wire transfer process. Confirm the escrow company’s wiring instructions directly by phone before sending any funds. Wire fraud is a real risk in real estate transactions.

- Use a proven negotiation approach when presenting your offer. Sellers respond better when buyers communicate clearly and professionally from the first conversation.

For investors building a repeatable acquisition process, understanding property acquisition strategies alongside cash offer mechanics gives you a real edge in competitive markets.

Key Takeaways

A cash offer gives sellers certainty and speed while giving buyers a competitive edge, but the 5%–15% price discount means sellers must weigh deal reliability against maximum price.

| Point | Details |

|---|---|

| Cash offer definition | A purchase using liquid funds with no mortgage, closing in 7–14 days. |

| Proof of funds requirement | Buyers must show liquid assets in checking, savings, or money market accounts. |

| Seller benefit | Removes lender contingencies, dramatically reducing the risk of deal failure. |

| Price trade-off | Cash buyers typically offer 5%–15% below market value in exchange for speed. |

| Move-out planning | Fast closings require sellers to negotiate leaseback agreements upfront. |

The part of cash offers most sellers overlook

Cash offers gained serious momentum during the early 2020s and have held their ground. About one in three home sales today closes without a mortgage. That tells me cash offers are no longer just an investor tool. Regular homeowners, retirees downsizing, and people inheriting property are all encountering them now.

What I have seen repeatedly is sellers making the same mistake: they fixate on the price gap and reject a solid cash offer for a financed offer that looks better on paper. Then the financed deal falls apart at the appraisal, and the seller is back at square one, often in a weaker negotiating position because the property has been sitting longer.

The sellers who make the best decisions treat certainty as a real dollar value. If a cash offer closes in 10 days and a financed offer closes in 45, that difference represents carrying costs, stress, and risk. Price those factors honestly before you decide.

I also want to be direct about the other side of this. Accepting a cash offer that is 15% below market value when you have no urgency is a mistake in the other direction. Cash buyers, especially investors, count on sellers not doing that math. Know your number. Know your timeline. Then negotiate from that position.

The sellers who get the best outcomes are the ones who understand what they are actually trading when they accept a cash offer. Speed and certainty are valuable. They are not priceless.

— Dave

ClosersLeague and the cash offer conversation

Real estate investors and wholesalers who make cash offers live and die by the quality of their seller conversations. Knowing what a cash offer is matters. Knowing how to present one to a motivated seller under pressure is a different skill entirely.

ClosersLeague builds that skill through AI-powered roleplay scenarios designed for real situations: inherited property, code violations, foreclosure, probate. You practice the exact conversations that lead to accepted cash offers, with feedback on your objection handling and tone. The inherited property cold calling practice module puts you in front of realistic seller scenarios so you arrive at every call prepared, not guessing. Stop winging your seller conversations. Start drilling them.

FAQ

What is a cash offer in real estate?

A cash offer is a purchase proposal where the buyer uses liquid funds to buy a property without a mortgage. No lender is involved, which removes financing contingencies and speeds up closing.

How does a cash offer work for the seller?

The seller receives a written offer along with a proof of funds letter. If accepted, the deal moves directly to escrow and closes in 7–14 days without a bank appraisal or underwriting process.

What is a cash buyer?

A cash buyer is any individual or entity that purchases real estate using liquid funds rather than a mortgage. Cash buyers include investors, flippers, retirees, and sellers of other properties who have freed up capital.

Do cash offers always win in a bidding war?

Cash offers win most competitive situations because they carry less risk and close faster, but a financed offer that is significantly higher can still win if the seller prioritizes maximum price over certainty.

Can you negotiate a cash offer?

Yes. Sellers can counter on price, contingencies, closing date, and leaseback terms. Cash buyers expect some negotiation, and sellers should always counter rather than accept or reject outright.